Are MCA Debt Relief Companies Legit? FTC and BBB Records

TL;DR — Key Facts

- →Some MCA debt relief operators are legitimate law firms doing real work. Others are unlicensed vendors that collect large upfront fees and deliver little. The category is mixed, not uniformly fraudulent.

- →The FTC Telemarketing Sales Rule (16 CFR § 310.4(a)(5)) bars debt-relief providers from collecting fees before settling at least one debt for consumer borrowers. Small business commercial debt sits in a gray area, which some operators exploit.

- →BBB has documented complaints involving MCA Resolve, LLC and MCA Debt Advisors, LLC where customers report paying $15,000 to $24,000 in upfront fees while creditors were never contacted.

- →The FTC distributed $3.3 million in March 2026 to 4,981 small businesses harmed by Yellowstone-brand MCA operators, the first commercial-borrower refund in an MCA enforcement action.

- →Four red flags disqualify a vendor: cold calls to your office, large upfront retainers ($5,000+) before any work begins, guaranteed reduction percentages, and DBA aliases that hide poor reviews.

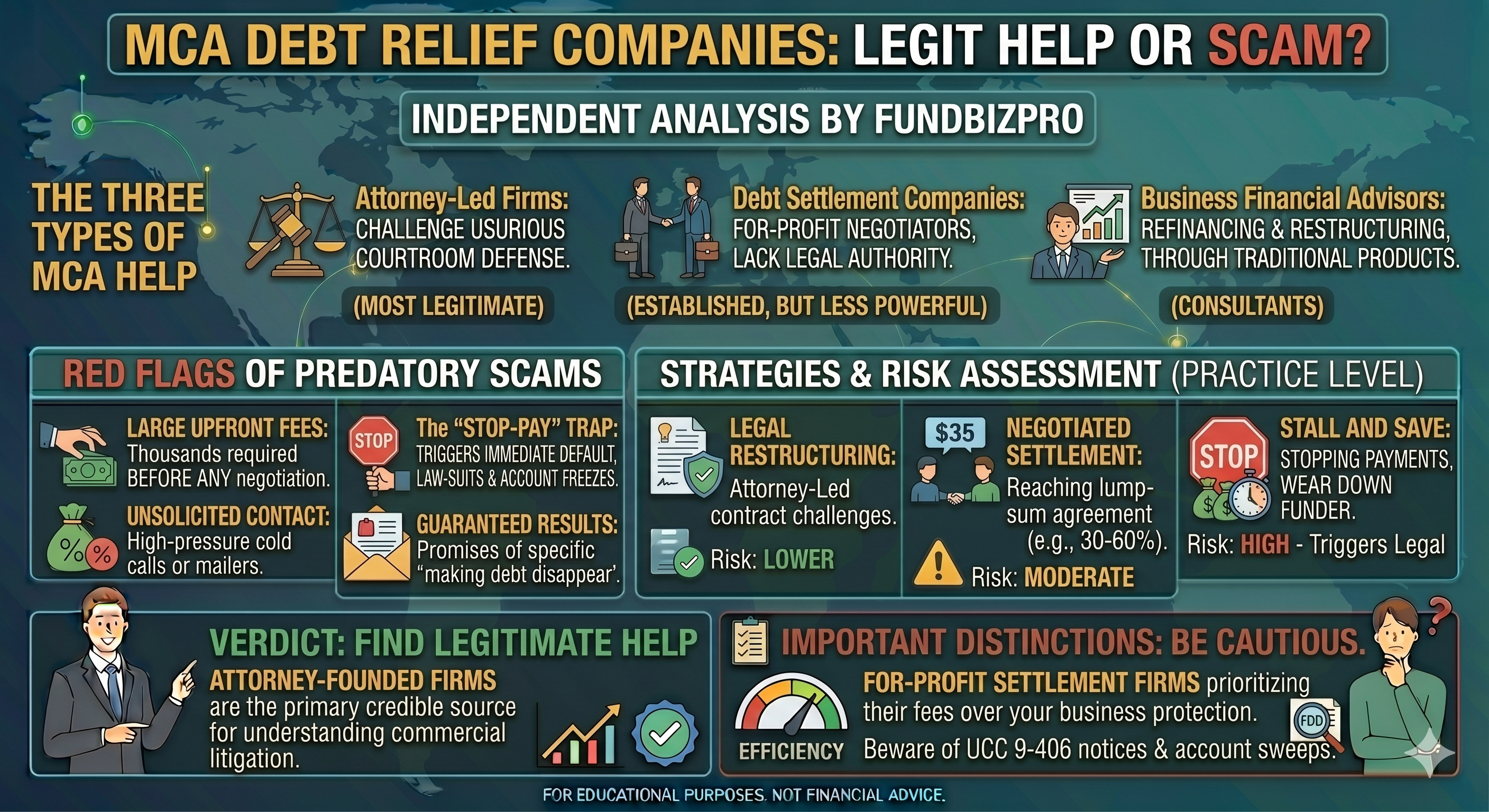

Direct answer: some are, most are not

The honest answer is mixed. A small number of MCA debt relief operators are licensed law firms with real attorneys doing real settlement work. A much larger number are unlicensed marketing vendors that collect upfront fees ranging from $5,000 to $20,000, contact creditors rarely or never, and disappear when complaints accumulate. The Federal Trade Commission has brought multiple enforcement actions against the latter group. The Better Business Bureau has documented complaint patterns at named operators including MCA Resolve, LLC (Delray Beach, FL) and MCA Debt Advisors, LLC (Erie, PA). Neither company is BBB-accredited as of this writing.

The distinction that matters: whether the entity you are paying is a law firm operating under attorney-client privilege, or a debt-settlement vendor that contracts loosely with attorneys to dress up its fee structure. The functional, legal, and outcome differences are large.

Trust signals: what to verify before paying anyone

Before sending any money, verify the entity against public records. The signals below are objective and free to check.

| Trust signal | What to look for | Where to verify |

|---|---|---|

| State bar registration | The lead attorney is admitted to your state bar | Your state bar directory (free public lookup) |

| BBB rating and accreditation | A or A+ accredited, low complaint volume | bbb.org search by company name |

| FTC enforcement history | No active or settled FTC actions | ftc.gov/legal-library/browse and ftc.gov/enforcement |

| State AG complaints | No pattern complaints with your state AG | Your state Attorney General website |

| Trustpilot / Google reviews | 4+ stars across multiple years, not just recent | trustpilot.com search |

| DBA aliases | Operator does business under multiple names | BBB profile lists alternative names |

| Upfront fee structure | Fees collected only after a debt is reduced and a payment is made | Written engagement letter |

The Better Business Bureau is not perfect, but it is useful as a starting filter. MCA Resolve, LLC has a documented BBB complaint history including reports of $24,000 collected in fees with employees acknowledging they had not yet contacted creditors. MCA Debt Advisors, LLC has a documented complaint history including reports of upfront fees followed by liens and lawsuits being placed against the customer rather than removed. Both companies are not BBB-accredited.

What users actually report

Reddit threads on r/loansforsmallbusiness and r/smallbusiness, Trustpilot reviews, and BBB complaint files surface a consistent pattern in the unlicensed vendor segment: customers pay several thousand dollars in fees over the first 30 to 90 days, the vendor stops returning calls between months 2 and 6, and creditors continue to pursue the original debt because no actual settlement was reached. Some customers report that the vendor used a different operating name (DBA alias) than the entity that solicited them, making complaints harder to file.

The complaint pattern at law firms with active MCA practices looks different. Customers report a paid initial consultation in the $200 to $500 range, a clear written engagement letter listing scope and fee structure, motion practice or settlement negotiation that produces a documented outcome (settlement letter, vacated judgment, released UCC lien), and the firm carrying its own state-bar regulated insurance. Disputes still happen, but the procedural footprint is materially different from the vendor pattern.

In March 2026, the FTC distributed $3.3 million in refunds to 4,981 small businesses harmed by MCA operators in the Yellowstone brand family, which the FTC originally sued in 2023. This was the first time the FTC directed money back to commercial borrowers in an MCA enforcement action. State and federal enforcement against MCA debt relief vendors has produced more than $1.6 billion in judgments, settlements, and debt cancellations between January 2025 and early 2026.

Four red flags that disqualify a vendor

These are not soft signals. Any one of them is enough to walk away.

Cold calls to your office. Legitimate law firms rarely cold-call distressed business owners. The FTC and multiple state AGs have flagged cold-call solicitation as a consistent marker of debt-relief fraud. If a vendor reached you first by an unsolicited call, treat the call as a sales pitch, not a service offer.

Large upfront retainers before any work begins. Demands for $5,000 to $20,000 up front, before reconciliation requests are sent, before any creditor is contacted, before any settlement is reached, are the single most consistent indicator of a vendor that does not intend to deliver. The FTC Telemarketing Sales Rule (16 CFR § 310.4(a)(5)) prohibits this structure for consumer debt relief and requires fees to be tied to actual settled debts. Small business commercial debt sits in a gray area where the rule does not strictly apply, which is why the abuse concentrates here.

Guaranteed reduction percentages. "We will cut your debt by 50 to 70 percent" is a sales claim, not a legal opinion. Real settlement outcomes depend on documented financial distress, available legal arguments, and the funder's litigation appetite. Any vendor that guarantees a percentage upfront is misrepresenting how settlements actually work.

DBA aliases that hide reviews. When a vendor operates under multiple names, it is often to outrun negative reviews. MCA Resolve, LLC has reportedly done business as "Resolve Capital Consolidation." Cross-check operator names on BBB and Google for alternate identities. If the same address or phone number appears under more than one brand, take the negative reviews under any of the names as relevant.

Better alternatives to a debt relief vendor

If you are considering an MCA debt relief vendor, the alternatives below produce documented outcomes at lower (or comparable) cost with materially better consumer protections.

| Alternative | Best for | Typical cost | Why it is a better fit |

|---|---|---|---|

| Licensed MCA-defense attorney | Borrowers in distress with multiple positions | $200 to $500 initial consultation, contingency or hourly thereafter | Attorney-client privilege, can file motions, raise usury defenses, vacate COJs |

| Free SBDC or state Small Business Development Center | Borrowers wanting independent guidance before paying anyone | Free | No fee, no sales incentive, can refer to vetted counsel |

| State Bar Lawyer Referral Service | Borrowers without an existing attorney relationship | Often $25 to $50 for initial consultation | Vetted attorneys, regulated under state bar rules |

| Direct reconciliation request to funder | Borrowers whose revenue dropped vs application | Free | The clause is already in your contract; written request creates documentation |

| Bankruptcy attorney consultation | Borrowers facing insolvency with no operating future | $200 to $500 initial consultation | Automatic stay halts collections immediately under 11 U.S.C. § 362 |

The MCA settlement pillar covers the attorney-led path in detail, including the difference between a settlement vendor and a law firm and what each can actually deliver. See the MCA settlement guide and the pillar on getting out of an MCA for the full framework.

Sources

- FTC: Halts Illegal Debt-Relief Operation Falsely Impersonating Businesses and Government (July 2025) ↗

- FTC: Companies and People Banned From Debt Relief ↗

- eCFR: 16 CFR § 310.4 Abusive Telemarketing Acts or Practices ↗

- BBB: MCA Debt Advisors LLC Complaints ↗

- BBB: MCA Resolve LLC Complaints ↗

- California DFPI: Debt Settlement Services Registration ↗

Read Next

Financing

MCA Settlement: How Attorneys Negotiate a Reduced Payoff

Reported MCA settlement recoveries run 40 to 70 percent of the outstanding balance. Here is the negotiating power that drives the number, the lump-sum vs installment trade-off, the timeline, and the 1099-C tax bill nobody warns you about.

Financing

How to Get Out of a Merchant Cash Advance

Five legitimate ways to exit an MCA in 2026, ranked by cost. SBA closed the refinance door in June 2025. Here is what still works, what to avoid, and what to do in the first 72 hours after a missed payment.

Financing

What Happens If You Default on a Merchant Cash Advance

MCA defaults escalate within 24 hours, not 30 days. Here is the real timeline: ACH retries, NSF stacking, acceleration, UCC enforcement, confession of judgment, and bank account freezes. Plus the 72-hour action plan that changes outcomes.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

Get the free MCA Vendor Vetting Checklist (the 7 records to verify before paying anyone)

Free guide — delivered to your inbox.

Frequently Asked Questions

Before you sign a lease, know what the data says about your address.

Score a franchise location free →By FundBizPro Editorial · Published 2026-05-05 · United States

Written by

FundBizPro Editorial Team

Backgrounds in commercial banking, SBA lending, and franchise industry research

The FundBizPro Editorial Team covers North American franchise costs, FDD analysis, site selection, and acquisition financing. Articles draw on current FDD filings and primary industry sources and are reviewed before publication. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →