Bank of America Small Business Loan: Rates, Requirements, and Alternatives (2026)

TL;DR — Key Facts

- →Bank of America is consistently among the top 5 SBA lenders by dollar volume - a genuine player, not a box-checker.

- →Business Advantage Term Loans: $10,000–$100,000 unsecured; $25,000–$250,000 secured. Existing BofA relationship required.

- →BofA SBA 7(a) loans go up to $5 million for acquisition and real estate financing.

- →Minimum credit score in practice: 670–700+ for term loans; 720+ for best rates and larger amounts.

- →The BofA Practice Solutions program is specifically built for healthcare, dental, and veterinary practice acquisition - a standout niche product.

What Bank of America actually offers small businesses

Bank of America's small business lending operation is large and legitimate. It processes more SBA loan volume than most banks and has dedicated teams for franchise financing, healthcare practice acquisition, and commercial real estate. For borrowers who qualify and bank with BofA, it's a reasonable first call.

The product line covers the expected range: SBA 7(a) loans, business term loans (secured and unsecured), business lines of credit, equipment financing, and commercial real estate loans. BofA has also developed niche programs - particularly Practice Solutions for healthcare businesses - that are genuinely well-designed for their target markets.

The limitations are similar to any large-bank lender: relationship requirements, volume-driven processing that reduces flexibility on complex files, and credit score floors that are higher in practice than the minimums SBA programs technically allow.

BofA small business loan product comparison

Quick reference for the products most relevant to franchise buyers and business acquisition:

| Product | Amount | Term | Key Requirement |

|---|---|---|---|

| Business Advantage Unsecured | $10K-$100K | 12-60 months | BofA checking + $100K annual revenue |

| Business Advantage Secured | $25K-$250K | Up to 5 years | Collateral + BofA checking |

| SBA 7(a) | Up to $5M | 10-25 years | 700+ credit, franchise eligibility |

| Practice Solutions | Up to $5M | Up to 10 years | Licensed professional (healthcare, dental, vet) |

| Business Line of Credit | $10K-$250K | Revolving | BofA checking, 2+ years in business |

The dividing line for most acquisition buyers: if you need more than $250,000, Business Advantage products don't reach that amount - SBA 7(a) is the path. If the acquisition is in healthcare or a professional practice, Practice Solutions competes directly with SBA on terms.

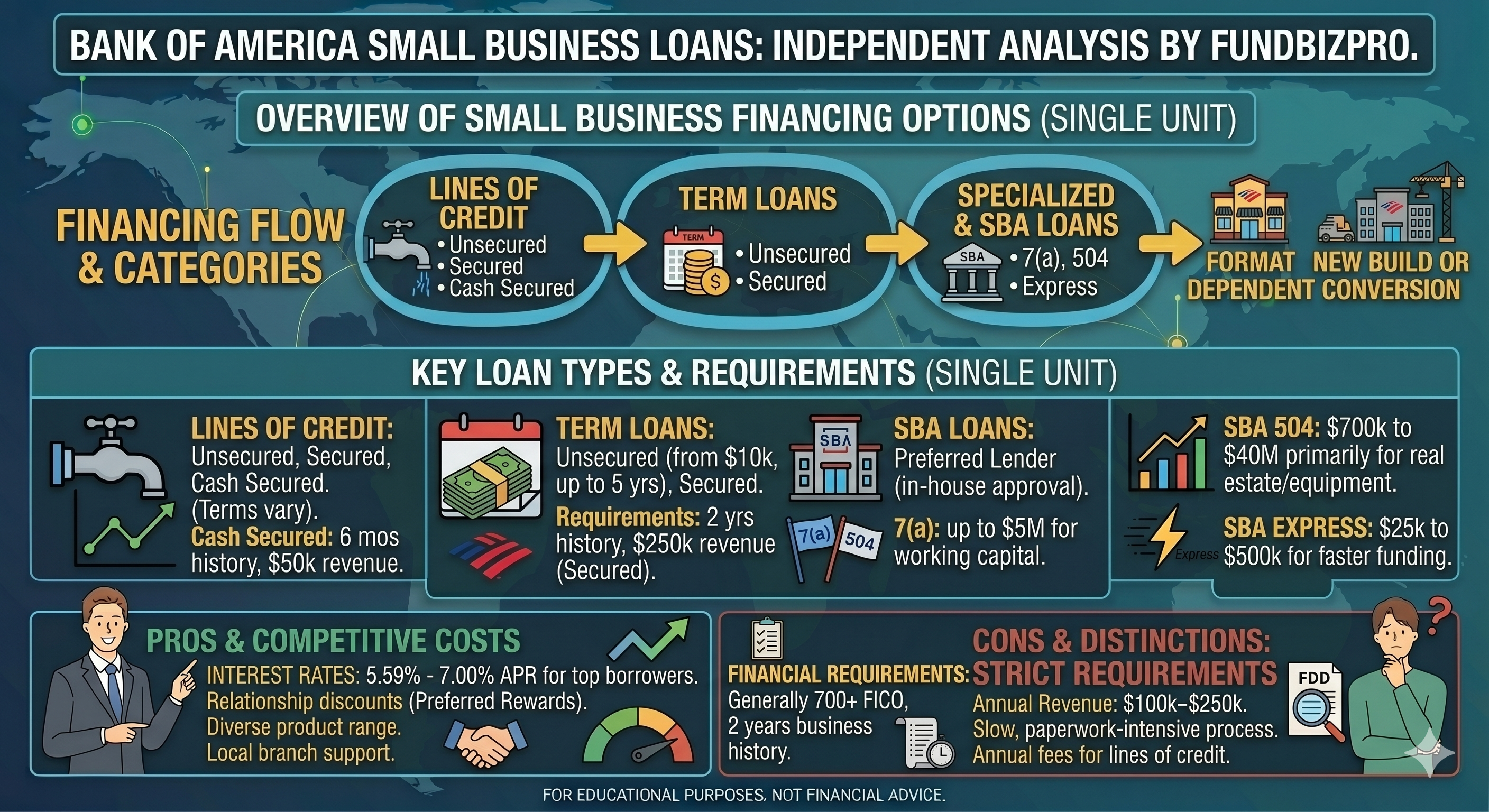

Business Advantage Term Loans: the main retail product

Bank of America's Business Advantage Term Loan is its primary small business lending product for existing BofA customers. Two tiers:

Unsecured (no collateral required): - Amount: $10,000–$100,000 - Terms: 12–60 months - Rates: variable; BofA does not publicly disclose rates, but expect 8%–18% for qualified borrowers in 2026 - Requirements: active BofA business checking account, 2+ years in business, $100,000+ annual revenue - No early repayment penalty

Secured (business assets as collateral): - Amount: $25,000–$250,000 - Terms: up to 5 years - Lower rates than unsecured tier - Requires collateral: equipment, inventory, or receivables

Both tiers require an existing BofA business banking relationship - this is non-negotiable, not a preference. If you don't bank with BofA, these products are not accessible until you open an account and establish a relationship.

For business acquisition financing above $250,000, the Business Advantage term loan is the wrong product - you need SBA 7(a) or commercial real estate financing.

BofA SBA 7(a) loans: the product for acquisition financing

For business acquisitions, franchise purchases, and larger financing needs, BofA's SBA 7(a) program is the relevant product. BofA is a top-5 SBA lender by dollar volume and an SBA Preferred Lender (PLP), meaning it can approve loans in-house.

BofA SBA 7(a) terms follow the program's standard structure: - Loans up to $5 million - Terms: 10 years (working capital/acquisition), 25 years (real estate) - Down payment: 10% minimum for qualified buyers - Rates: within SBA regulated caps (prime + 2.75%–4.75% for loans above $350,000) - Franchise Registry: BofA has experience with registered franchise brands

BofA SBA tends to be most efficient when the file is clean: established business with 2+ years of tax returns, 700+ credit score, relevant experience, and a recognized franchise brand. Complex files - industries BofA is cautious about, credit in the 670–690 range, deal structures with multiple moving parts - can stall in BofA's volume-processing environment.

For straightforward franchise acquisitions by experienced buyers with strong credit, BofA SBA competes well. For deals that need an underwriter who will advocate for the file, a community SBA lender often serves better.

Practice Solutions: the standout niche product

Bank of America's Practice Solutions program is worth knowing about specifically for buyers in healthcare, dental, optometry, veterinary, and chiropractic practices. It's one of the better-designed niche lending programs at a large bank, with terms specifically calibrated for the professional practice acquisition market.

Practice Solutions features: - Loan amounts: up to $5 million - Terms: up to 10 years - Financing for practice acquisition, partnership buy-ins, equipment, real estate, and working capital - Streamlined underwriting for licensed professionals with verifiable income history - No collateral required up to certain loan sizes (backed by the professional's license and revenue)

Why this matters: healthcare and veterinary practice acquisitions have specific financial characteristics - stable recurring revenue, low customer concentration, licensing that creates real barriers to competition - that generic SBA underwriting doesn't always recognize. Practice Solutions is built around these characteristics.

If you're buying a dental, veterinary, or medical practice, BofA Practice Solutions deserves a direct conversation alongside SBA alternatives.

Business Line of Credit

BofA's business lines of credit run from $10,000 to $100,000 for unsecured products, with secured options up to $250,000. Requirements mirror the term loan: active BofA business checking, 2+ years in business, $100,000+ annual revenue.

The revolving structure works well for working capital cycling - covering gaps between invoices and payments, managing inventory purchasing, bridging seasonal fluctuations. It is not suited for acquisition financing.

BofA does offer a Business Advantage Unlimited Cash Rewards Mastercard with credit limits up to $250,000 - useful for business expenses and cash flow management, not for capital-intensive acquisitions.

What most articles get wrong about BofA business loans

Most articles list SBA program minimums and stop there. The SBA minimum credit score is 650 - but BofA's practical threshold for SBA 7(a) approval on an acquisition is 700-720+. That gap filters out a significant share of borrowers who read the published requirements and believe they qualify.

The relationship requirement gets consistently underreported. Nearly every BofA small business product - unsecured loans, secured loans, lines of credit - requires an active BofA business checking account. Articles describe products as if they're open to all applicants. They aren't. Without an active BofA checking account, the Business Advantage products are closed to you until you open an account and build a 3-6 month relationship history.

Approval timelines are also routinely described as fast. Those numbers assume a clean file - existing customer, strong credit, complete documentation, straightforward deal structure. Files with any complexity push past those estimates quickly.

When BofA is the right choice - and when it isn't

Bank of America makes sense when: - You already have an active BofA business banking relationship - You're buying a healthcare, dental, or veterinary practice (Practice Solutions) - You have 700+ credit and clean, complete financials - You want a large institutional SBA lender with franchise-specific experience - Your deal is straightforward and doesn't need creative underwriting

Look elsewhere when: - You don't have a BofA business banking relationship (all BofA products are essentially closed to you without one) - Your credit is below 690 (community SBA lenders are more flexible) - Your deal is complex and needs an underwriter who will advocate - You're buying an independent restaurant or other high-scrutiny industry (BofA is conservative here) - You want local service and a banker who returns calls quickly

An often-missed alternative: Live Oak Bank is a specialty SBA lender with no branch network and laser-focused on specific industries (veterinary, dental, self-storage, funeral homes, franchises). For industry-specific deals, Live Oak often produces better terms and faster processing than BofA because they know the industry deeply.

Read Next

Financing

Chase Small Business Loans: What You Get and What They Don't Tell You

Chase small business loans explained: relationship requirements, SBA 7(a) limits, real credit thresholds, and when a community bank serves you better.

Financing

Wells Fargo Small Business Loan: Rates, Requirements, and Better Alternatives

Wells Fargo small business loan products are limited — SBA capacity shrank post-2016 and hasn't recovered. Here's what works and who should look elsewhere.

Guide

How Do You Buy a Business? A Plain-English Walkthrough

Learn how do you buy a business in plain English: SBA loans, due diligence, the Letter of Intent, and the location check most buyers skip before closing.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

Before you approach any lender, know what your location can support - score any address free.

Free guide — delivered to your inbox.

Frequently Asked Questions

Before you sign a lease, know what the data says about your address.

Score a franchise location free →Score a Location

By FundBizPro Research · Published 2026-04-18 · United States

Written by

FundBizPro Research Team

Backgrounds in commercial banking and SBA lending

The FundBizPro Research Team writes from primary sources - government program documentation, SBA SOP language, lender-published rate sheets, and FDD filings - rather than aggregating other websites. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →