Is BriteCap Financial Legit? An Honest Review

TL;DR — Key Facts

- →BriteCap Financial is a licensed direct lender, not a broker - you deal with one company start to finish

- →Focused on small businesses with 12+ months in business, $100K+ annual revenue, and 600+ credit score

- →Products: short-term business loans and lines of credit, $10,000–$250,000, terms up to 24 months

- →APR range: approximately 20%–75%; BriteCap discloses APR upfront, a transparency advantage over most alternative lenders

BriteCap

United States

Efficiency Score

6.8/10

APR Range

20–75%

Funding

2 days

Min Credit

600+

Is BriteCap a Real Company?

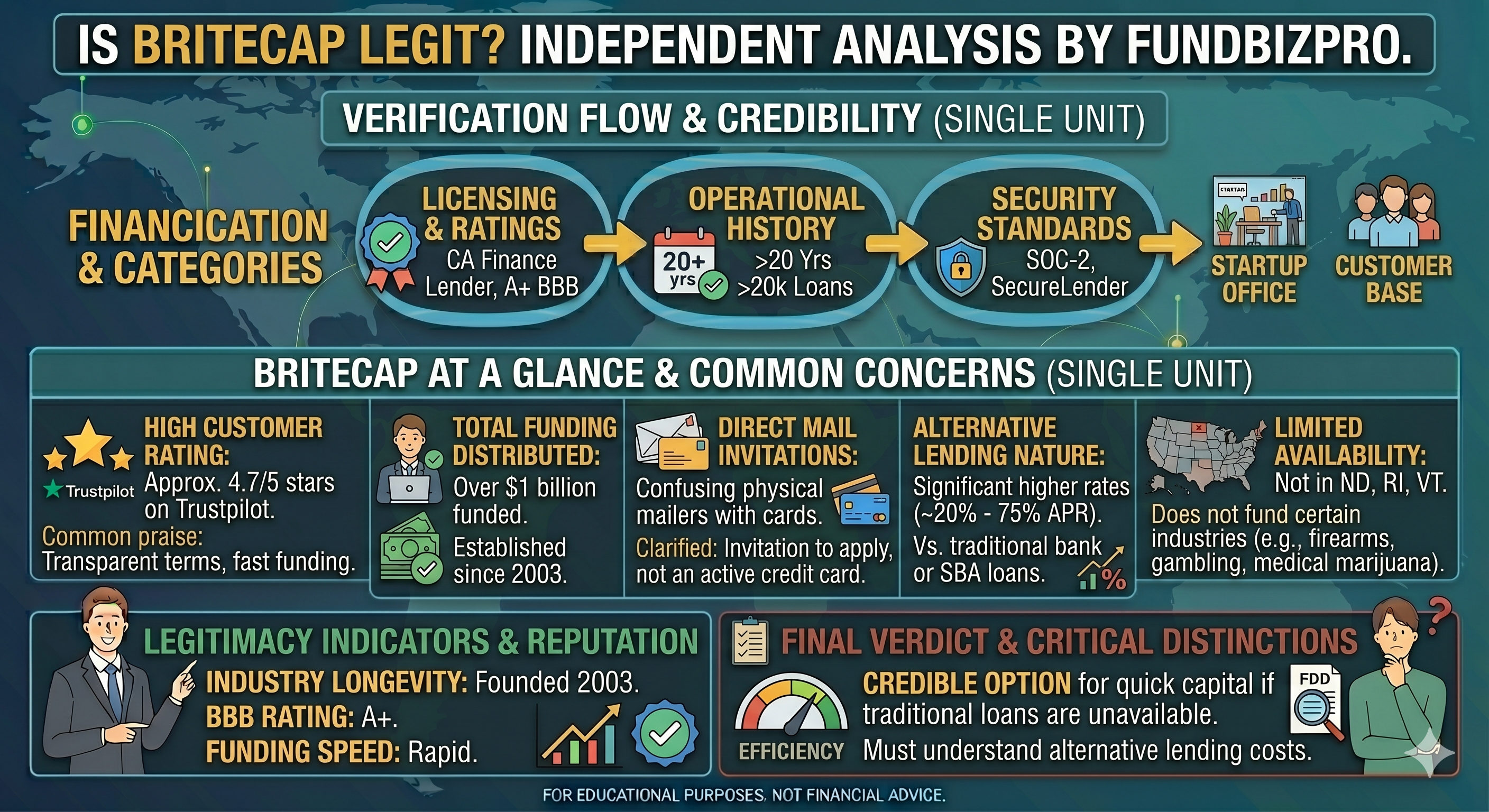

Yes. BriteCap Financial LLC is a licensed commercial lender based in Chicago, Illinois. It operates as a direct lender - meaning it funds loans from its own capital rather than brokering to other lenders. This is an important distinction: you will negotiate, sign, and repay with BriteCap directly.

BriteCap has been operating since 2015 and maintains active state lending licenses. It is registered with the Better Business Bureau, though it is not BBB-accredited as of 2025. There are no state regulatory actions or consumer protection violations on record from public databases.

| Trust Signal | Status |

|---|---|

| BBB status | Registered, not accredited; no unresolved complaints on record (2025) |

| Year founded | 2015 |

| Headquarters | Chicago, Illinois |

| Lender type | Direct lender - funds from own capital, not a broker |

| State lending licenses | Active in required states; confirm your state before applying |

| CFPB database | Not applicable - CFPB tracks consumer lenders, not commercial |

| Trustpilot reviews | Publicly available; speed and transparent pricing cited most frequently |

What BriteCap Actually Offers

BriteCap specializes in two products:

Short-term business loans: Lump-sum funding repaid over 4–24 months via daily or weekly ACH withdrawals from your business checking account. No prepayment penalties on most products.

Business lines of credit: Draw-as-needed credit lines up to $250,000. Interest accrues only on drawn amounts. Useful for working capital cycles where cash needs are unpredictable.

Minimum requirements: - 12+ months in business - $100,000+ annual revenue - 600+ personal credit score - Active business checking account

BriteCap does not do equipment financing, SBA loans, or real estate loans. Its niche is fast working capital for businesses that need cash in 24–72 hours.

Understanding BriteCap's Pricing

Unlike most alternative lenders, BriteCap discloses APR upfront on its term loan products - a meaningful transparency advantage. Early repayment on term loans reduces total interest owed, which is not the case with factor-rate products.

Some short-term products in this lending segment use factor rates instead of APR - so if any offer you receive quotes a factor rate, convert it: a $50,000 advance at a 1.30 factor rate means you repay $65,000 total regardless of payoff speed. Over 12 months that is approximately 60% APR; over 6 months, approximately 120% APR. Always confirm whether your specific BriteCap offer is APR-based or factor-rate-based before signing.

BriteCap's rates are consistent with its peer group (Fora Financial, OnDeck, SBG Funding) for comparable borrower profiles. The no origination fee and APR disclosure make it one of the more transparent options in the segment.

What Borrowers Say

Reviews on Trustpilot, Google, and threads on r/loansforsmallbusiness and r/smallbusiness show a consistent pattern: borrowers praise speed and upfront pricing, and flag two specific problems.

Positive: same-day or next-day funding after approval, no surprise fees, APR disclosed before signing. These are not universal in the alternative lending market.

Negative: (1) daily ACH withdrawals straining cash flow when revenue dips - a fixed daily pull does not adjust to your actual revenue. (2) Renewal offers that reset the total payoff - borrowers who roll over before the existing loan is cleared end up paying interest on both old and new principal.

The renewal trap is real. If BriteCap calls to offer a "renewal" before you have fully paid off the current loan, calculate the net new cash you receive versus total repayment of the new loan before accepting. The math often surprises borrowers who focus on the new lump sum rather than the total cost.

Red Flags to Watch

BriteCap itself is not a red flag. But four things warrant attention when reviewing any BriteCap offer:

1. Factor rate vs. APR confusion. BriteCap discloses APR on term loans, but some MCA-adjacent products use factor rates. If your offer letter shows a "factor" or "purchase price" rather than an APR, convert before signing. A 1.30 factor on $50,000 over 6 months is approximately 120% APR. 2. Renewal call before 60% payoff. Receiving a renewal offer before you have paid down at least 60% of the original balance means you will be paying interest on rolled-over principal from the prior loan. 3. Daily ACH on a business with variable revenue. ACH withdrawals do not pause when your business has a slow week. A restaurant or retail business with seasonal revenue will have failed pulls, NSF fees ($25–$50 each), and potential acceleration of the loan. 4. Loan stacking. BriteCap does not explicitly prohibit taking a second short-term loan from another lender, but carrying multiple daily-ACH obligations simultaneously is the most common path to default in this lending category. Avoid it.

Verdict

BriteCap is a legitimate lender with a clear niche: fast capital for businesses that cannot access bank or SBA financing. If you have 600+ credit, $100K+ in annual revenue, and 12+ months of operating history, BriteCap is a viable option for funding in under a week.

Use it when: You need capital faster than any bank can move, you have a specific short-term need (inventory, payroll bridge, equipment repair), and you have run the numbers on the total repayment cost.

Do not use it when: You are carrying other short-term debt (stacking is dangerous), when revenue is inconsistent (daily ACH is unforgiving), or when you qualify for SBA or a bank LOC (BriteCap is 3–5x more expensive on cost of capital).

Read Next

Lender Review

BriteCap Review: Transparent Pricing in the Alternative Lending Market

BriteCap review: no origination fee, 20%-75% APR, and who it suits best. What competitors don't tell you about their origination fees.

Lender Review

OnDeck Review: Fast Funding with a Real Cost

An independent OnDeck review covering rates (27%–99% APR), qualification requirements, Reddit sentiment, and exactly who should - and should not - use it.

Legitimacy

Is BusinessLoans.com Legit? An Honest Review

An honest look at BusinessLoans.com - what it is, how it works, what it costs, and whether you should use it for your small business loan.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

Check your loan readiness before you apply →

Free guide — delivered to your inbox.

Frequently Asked Questions

Answer 10 questions. See which lenders match your profile and what loan types fit.

Check your loan readiness →By FundBizPro Research · Published 2025-02-17 · Updated 2025-05-01 · United States

Written by

FundBizPro Research Team

Backgrounds in commercial banking and SBA lending

The FundBizPro Research Team writes from primary sources - government program documentation, SBA SOP language, lender-published rate sheets, and FDD filings - rather than aggregating other websites. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →