SBG Funding Review: High Loan Amounts and Multiple Product Options

TL;DR — Key Facts

- →SBG Funding offers loans up to $5M - the highest of any alternative lender reviewed.

- →Minimum requirements: 550 credit, $120K annual revenue, 6 months in business.

- →APR range: approximately 15%–80%; revenue-based financing available alongside term loans.

- →Origination fee applies; funding in 2 business days.

- →Strongest use case is established businesses ($500K+ revenue) that have outgrown OnDeck's $250K cap.

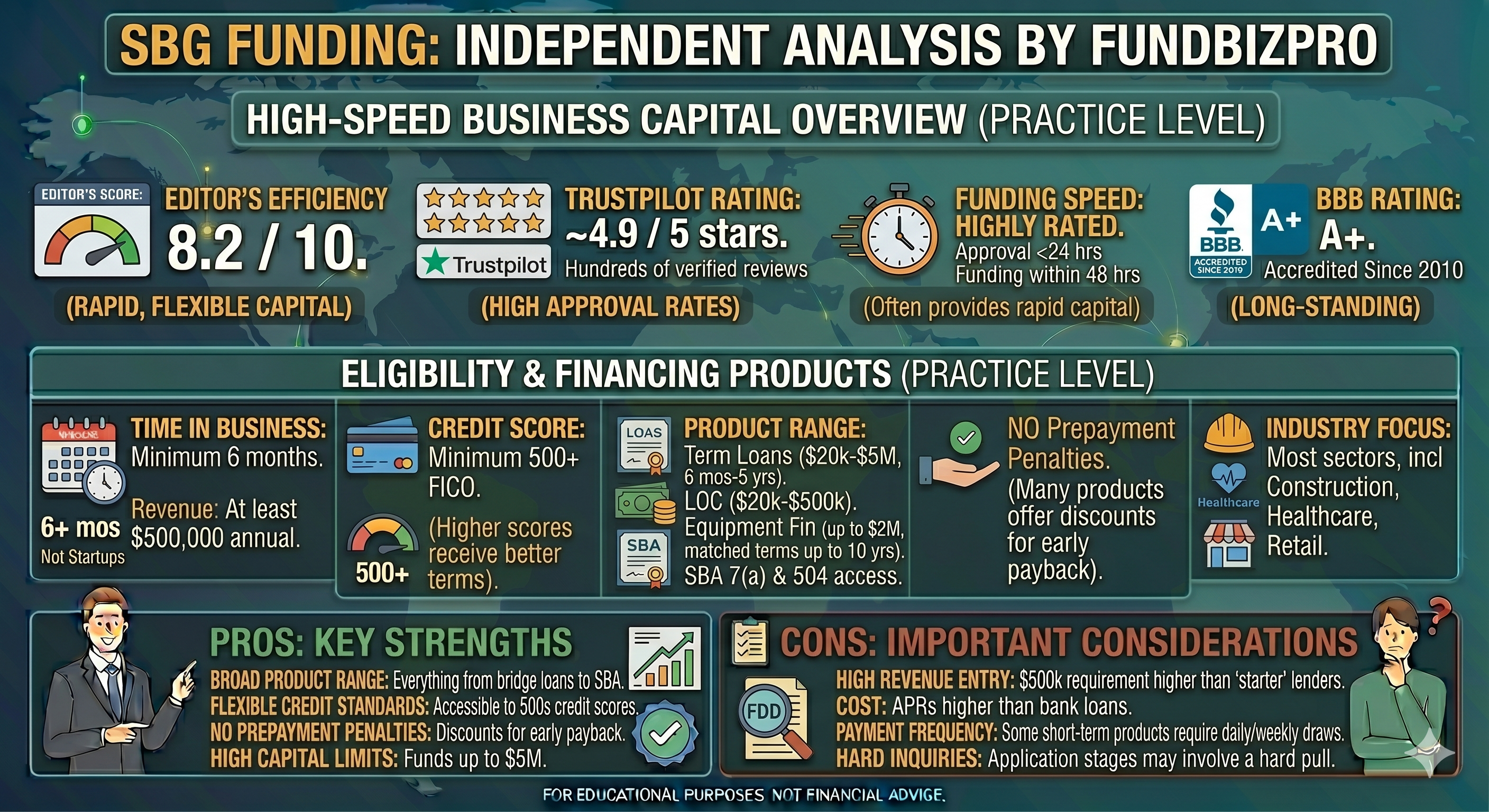

SBG Funding

United States

Efficiency Score

6.8/10

APR Range

15–80%

Funding

2 days

Min Credit

550+

Verdict

SBG Funding stands out from most alternative lenders for one reason: the $5M loan cap. For established businesses with $500K+ in annual revenue that need more capital than OnDeck can provide (max $250K), SBG Funding fills a genuine gap. The 550 credit minimum also makes it accessible to borrowers who cannot clear OnDeck's 625 threshold. Rates are high relative to banks and SBA, but competitive within the alternative lending segment.

SBG Funding at a glance

| Feature | Details |

|---|---|

| Loan amount | $10,000 – $5,000,000 |

| Min credit score | 550 |

| Min annual revenue | $120,000 |

| Min time in business | 6 months |

| APR range | ~15% – 80% |

| Funding speed | 2 business days |

| Origination fee | Yes |

| Prepayment penalty | None |

What the website does not tell you

Large loan amounts require much stronger profiles than the minimums suggest. The $5M ceiling is real - but accessing $1M+ requires multiple years of strong revenue, excellent credit, and significant collateral. A 550 credit score borrower should expect offers in the $25K–$100K range, not millions.

Revenue-based financing repayment fluctuates. SBG Funding offers revenue-based financing (RBF) alongside traditional term loans. RBF repayment is tied to a percentage of monthly revenue - appealing in slow months, but the total cost of capital is often higher than a fixed-rate term loan for the same amount. Understand which product you are being offered.

The origination fee compounds on rollovers. If you take a second loan while the first is outstanding - or roll over a maturing loan - the origination fee applies again. Frequent borrowers should model the total cumulative cost including origination across multiple facilities.

FundBizPro Efficiency Score

Speed: 8/10 - 2-business-day funding is consistently reported and competitive in the alternative lending market.

Cost: 5/10 - APR range of 15%–80% is meaningfully better at the low end than most alternative lenders, but the 80% ceiling still represents high-cost capital. Established businesses with strong profiles can access rates in the 15%–35% range.

Accessibility: 8/10 - 550 credit, 6 months history, $120K revenue. This is more accessible than OnDeck and CapFront while still requiring meaningful operating history.

Transparency: 6/10 - APR is disclosed on most products; revenue-based financing terms require additional clarity. Rates are risk-based and the range is wide, so the disclosed range is less informative than a specific quote.

Composite: 6.8 / 10

Reddit reality check

SBG Funding receives less Reddit coverage than OnDeck or Fora Financial, which likely reflects its more business-focused (rather than consumer-facing) marketing. The mentions that do appear focus on the loan amount ceiling - borrowers who had maxed out OnDeck's $250K cap mention SBG as the next step up. Complaints focus on origination fees eating into the effective loan amount and on revenue-based financing being more expensive than expected once the implied APR is calculated.

Who SBG Funding is right for

Good fit: An established HVAC company with $700,000 in annual revenue, a 580 credit score, and a need for $400,000 to purchase a fleet vehicle and expand operations. This is where SBG Funding genuinely serves a need that OnDeck cannot - the combination of scale and slightly relaxed credit requirements.

Wrong fit: Startups or very early-stage businesses. SBG Funding's large loan amounts and strong underwriting infrastructure are calibrated for established businesses. Businesses under 12 months old or below $200K revenue should consider Fora Financial or Advance Funds Network for their first capital access.

Three things to do before you apply

- Clarify whether your offer is a term loan or revenue-based financing - the total cost of capital calculation is fundamentally different for each.

- If you need over $250K, compare SBG Funding against Funding Circle ($25K–$500K, lower rates for 660+ credit) before accepting.

- For amounts under $200K with 600+ credit, also request quotes from OnDeck and CapFront to ensure you are getting a competitive rate.

Read Next

Lender Review

OnDeck Review: Fast Funding with a Real Cost

An independent OnDeck review covering rates (27%–99% APR), qualification requirements, Reddit sentiment, and exactly who should - and should not - use it.

Lender Review

Fora Financial Review: Accessible Capital, at a Price

Independent Fora Financial review - rates, MCA vs. term loan distinction, Reddit sentiment, and who should apply versus look elsewhere.

Lender Review

CapFront Review: Lower Rates, Stricter Requirements

Independent CapFront review - rates (12%–65% APR), qualification requirements, efficiency score, and how it compares to OnDeck and SBG Funding.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

See if your revenue and credit qualify for SBG Funding

Free guide — delivered to your inbox.

Frequently Asked Questions

Answer 10 questions. See which lenders match your profile and what loan types fit.

Check your loan readiness →By FundBizPro Research · Published 2026-05-03 · United States

Written by

FundBizPro Research Team

Backgrounds in commercial banking and SBA lending

The FundBizPro Research Team writes from primary sources - government program documentation, SBA SOP language, lender-published rate sheets, and FDD filings - rather than aggregating other websites. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →