SharpShooter Funding Review: Fast Capital for Canadian Small Businesses

TL;DR — Key Facts

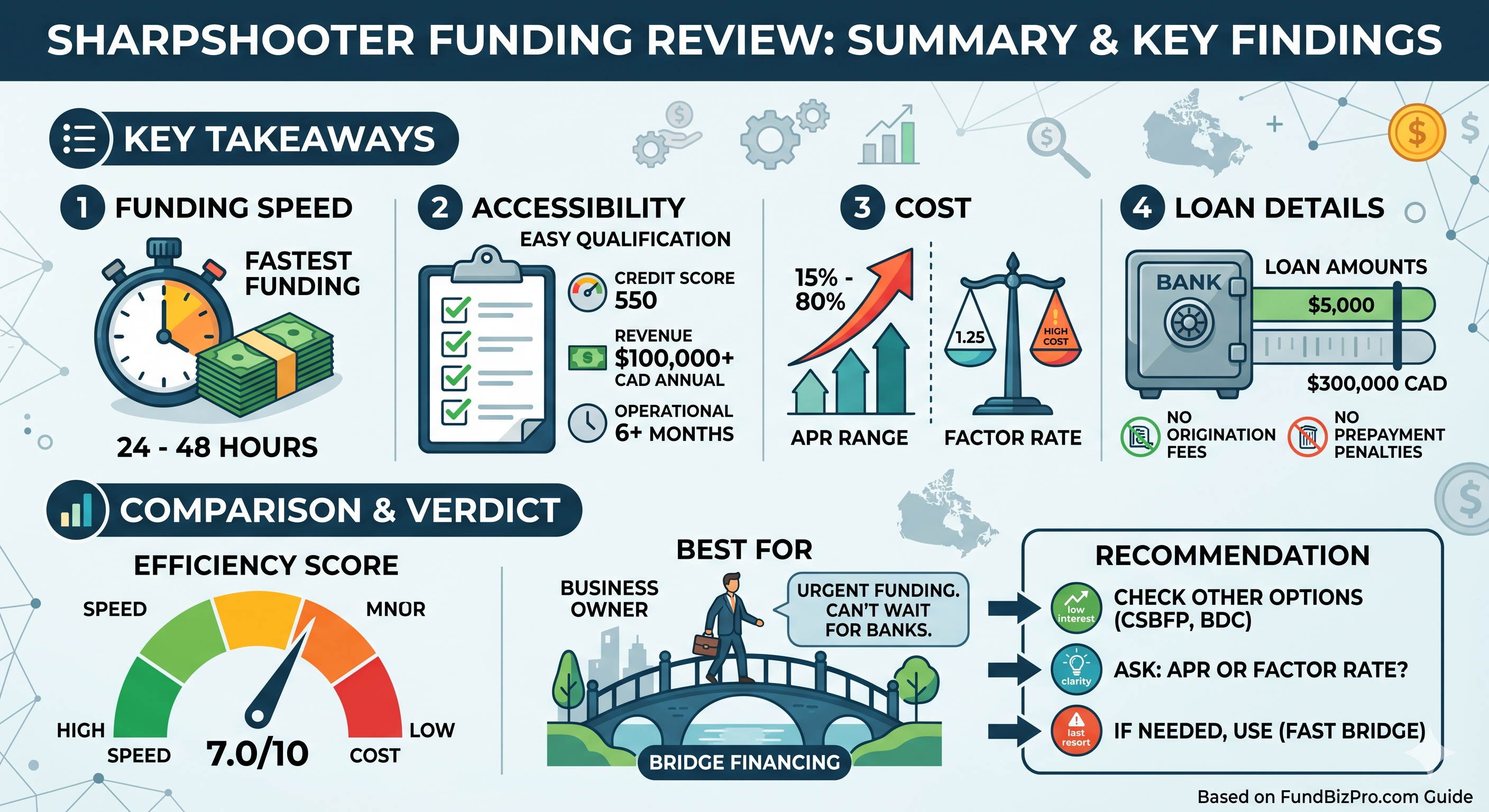

- →SharpShooter Funding funds in as fast as 24–48 hours - the fastest approval timeline among Canadian alternative lenders reviewed.

- →Minimum requirements: 550 credit score, $100,000 CAD annual revenue, 6 months in business.

- →APR range: approximately 15%–80%; some products use factor rates - always ask for APR equivalent.

- →No origination fee; no prepayment penalty on term loans.

- →Best for Canadian small businesses that have been declined by their primary bank and need capital quickly.

SharpShooter Funding

Canada

Efficiency Score

7.0/10

APR Range

15–80%

Funding

2 days

Min Credit

550+

Verdict

SharpShooter Funding is the most accessible and fastest among the four Canadian alternative lenders reviewed. For Canadian small businesses with 550+ credit, 6+ months of history, and $100K+ revenue that need capital in under a week, SharpShooter is the first call to make. The cost is high relative to CSBFP or BDC rates - but significantly lower than predatory MCA providers operating in Canada.

SharpShooter Funding at a glance

| Feature | Details |

|---|---|

| Market | Canada |

| Loan amount | $5,000 – $300,000 CAD |

| Min credit score | 550 |

| Min annual revenue | $100,000 CAD |

| Min time in business | 6 months |

| APR range | ~15% – 80% |

| Funding speed | 1–2 business days |

| Origination fee | None |

| Prepayment penalty | None |

What the website does not tell you

Factor rates are used on some products. SharpShooter offers both term loans and merchant cash advance-style products. The MCA products use factor rates (e.g., 1.25), not APR. A 1.25 factor rate on $40,000 means repaying $50,000 regardless of payoff timeline. Always ask: "Is this product priced on APR or a factor rate?"

Province availability may vary. SharpShooter Funding is headquartered in Ontario. Borrowers in some provinces may face different regulatory requirements or reduced product availability. Confirm your province is fully served before investing time in the application.

No origination fee is a genuine advantage. At $100,000, a 3% origination fee equals $3,000 - money that goes to the lender before you see a dollar. SharpShooter's no-fee structure means the full approved amount reaches your account, which is a meaningful advantage for borrowers working close to their capital minimums.

FundBizPro Efficiency Score

Speed: 9/10 - 24–48 hour funding is the fastest in the Canadian alternative lending market. For urgency-driven borrowers, this is SharpShooter's primary selling point.

Cost: 4/10 - 15%–80% APR is high relative to CSBFP (~prime + 3%) or BDC rates. However, it is competitive within the Canadian alternative lending market, where some operators charge 120%+ effective APR. No origination fee partially offsets the rate differential.

Accessibility: 9/10 - 550 credit minimum and 6-month history make SharpShooter the most accessible direct Canadian lender reviewed. The $100K revenue minimum is the primary qualification bar.

Transparency: 6/10 - APR is disclosed on term loan products, but the factor rate / APR distinction requires borrowers to ask specifically. The no-fee structure is clearly communicated, which adds transparency points.

Composite: 7.0 / 10

Reddit reality check

SharpShooter Funding appears in Canadian small business discussions on r/smallbusiness and r/canada. The consistent pattern: borrowers who had been declined by TD, RBC, or their primary bank used SharpShooter as a bridge financing option and were funded within 2 business days. The complaints focus on factor rates for MCA products being presented without explicit APR disclosure - the same issue that affects most alternative lenders in this segment.

Who SharpShooter Funding is right for

Good fit: A Toronto-area café chain with 8 months of operating history, $115,000 in annual revenue, and a 560 credit score (reduced by a business dispute two years prior) that needs $35,000 for kitchen equipment before a summer busy season. SharpShooter's 48-hour funding and 550 credit minimum make it one of the few options available to this borrower.

Wrong fit: Any Canadian business that qualifies for the Canada Small Business Financing Program (CSBFP) should exhaust that option first - CSBFP rates run at prime + 3% (approximately 9%–10%) versus SharpShooter's 15%–80% range. The CSBFP approval timeline is 2–4 weeks - a trade-off worth making for most non-urgent capital needs.

Three things to do before you apply

- Ask specifically: "Is this a term loan with APR, or a factor-rate product?" Get the answer in writing before accepting any offer.

- Check your CSBFP eligibility first - if your business meets the requirements ($10M or less in revenue, eligible industry), the CSBFP rate is 60–70 percentage points below SharpShooter's mid-range.

- Compare SharpShooter's offer with Journey Capital and Merchant Growth: three quotes from different Canadian alternative lenders takes less than a day and can save significant money.

Read Next

Lender Review

Journey Capital Review: Canadian Working Capital with Flexible Repayment

Independent Journey Capital review - rates, repayment flexibility, qualification requirements for Canadian businesses, and how it compares to SharpShooter and Merchant Growth.

Lender Review

Merchant Growth Review: No Collateral, Revenue-Based Financing in Canada

Independent Merchant Growth review - revenue-based financing, rates, qualification for Canadian retail and restaurant businesses, and how it compares to other Canadian lenders.

Lender Review

Driven Review: The Most Bank-Like Alternative Lender in Canada

Independent Driven review - lower rates (12%–60% APR), Canadian term loans, qualification requirements, and when it beats BDC or SharpShooter for established Canadian businesses.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

Check your readiness for SharpShooter or other Canadian lenders

Free guide — delivered to your inbox.

Frequently Asked Questions

Answer 10 questions. See which lenders match your profile and what loan types fit.

Check your loan readiness →By FundBizPro Research · Published 2026-05-03 · Canada

Written by

FundBizPro Research Team

Backgrounds in commercial banking and SBA lending

The FundBizPro Research Team writes from primary sources - government program documentation, SBA SOP language, lender-published rate sheets, and FDD filings - rather than aggregating other websites. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →