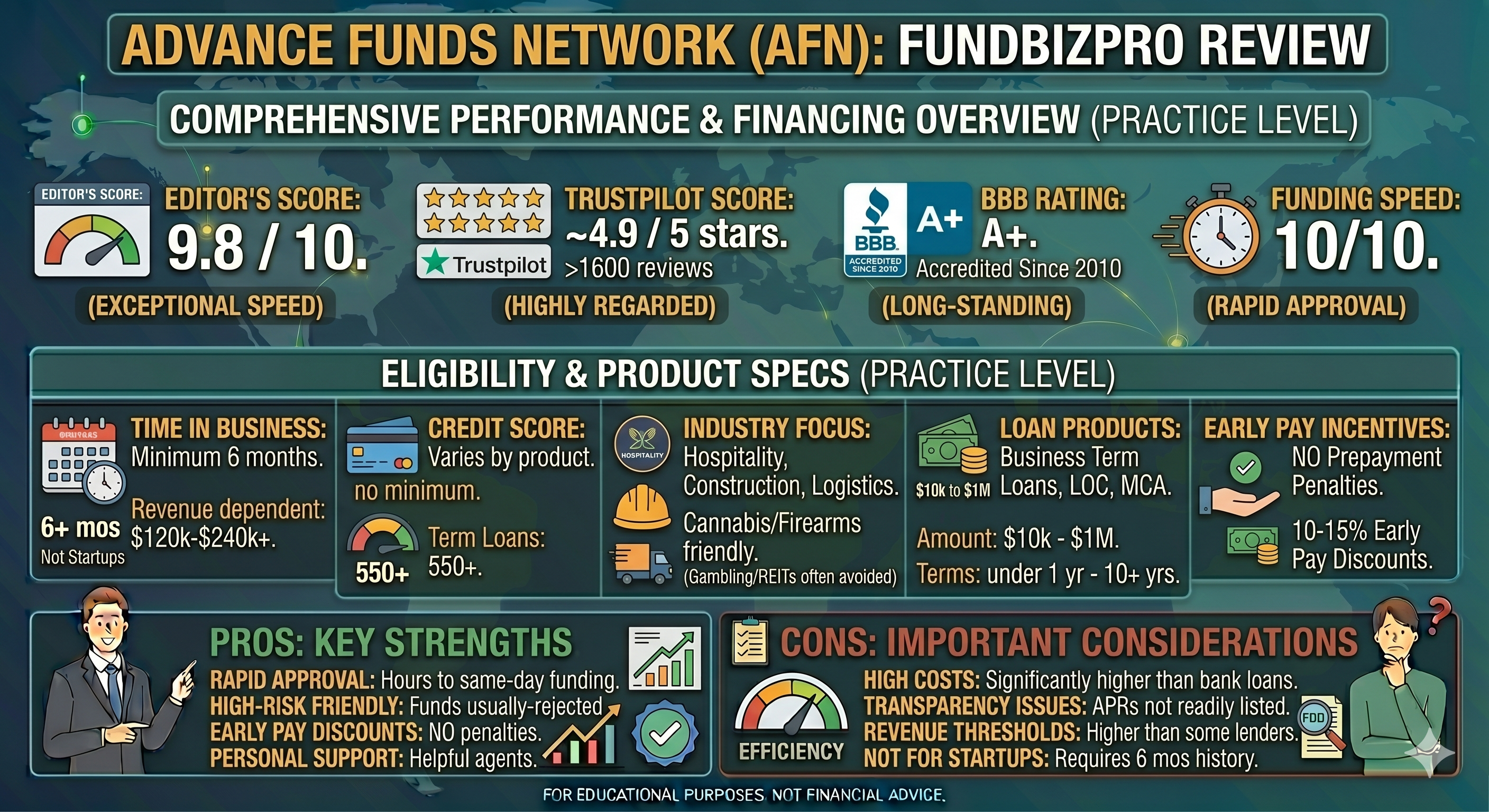

Advance Funds Network Review: Wide Access, High Cost

TL;DR — Key Facts

- →Advance Funds Network is a broker marketplace - it connects you with lenders, not a direct lender itself.

- →Accepts credit scores as low as 500 with 6 months in business and $120K annual revenue.

- →APR range is wide (18%–120%+) because the network includes very high-cost lenders for low credit profiles.

- →No origination fee from AFN itself - but individual lenders in the network may charge their own fees.

- →Funding in 1–2 business days for approved applications.

Advance Funds Network

United States

Efficiency Score

6.3/10

APR Range

18–120%

Funding

2 days

Min Credit

500+

Verdict

Advance Funds Network is not a lender - it is a broker that routes your application to lenders in its network. That distinction matters because AFN earns a referral fee from whichever lender funds your loan, creating an incentive structure that does not always align with getting you the best rate. For borrowers who have been declined everywhere else, AFN's 500 credit minimum provides a last resort. For anyone with 600+ credit, direct lenders will almost always produce better terms.

Advance Funds Network at a glance

| Feature | Details |

|---|---|

| Type | Broker/marketplace (not a direct lender) |

| Loan amount | $5,000 – $2,000,000 |

| Min credit score | 500 |

| Min annual revenue | $120,000 |

| Min time in business | 6 months |

| APR range | ~18% – 120%+ (varies by lender) |

| Funding speed | 1–2 business days |

| Origination fee | Varies by lender |

| Prepayment penalty | Varies by lender |

What the website does not tell you

AFN earns a referral fee from lenders, not from you - in theory. In practice, broker fees are often built into the rate you receive from the network lender. You are not seeing a neutral comparison of options - you are seeing options from lenders who pay AFN for referrals.

The 500 credit floor means high-cost lenders. No lender profitably approves a 500 credit score at 18% APR. The low end of AFN's rate range applies to the strongest borrowers in their network; a 500 credit score borrower should expect 60%–120% APR from any lender willing to fund them.

Factor rates are common in the AFN network. Many of the lenders AFN routes to use factor rates rather than APR, particularly for MCA products. This makes apples-to-apples cost comparison impossible without explicitly requesting APR from each lender.

FundBizPro Efficiency Score

Speed: 9/10 - Broker model allows AFN to route to whichever lender in the network can fund fastest. 24-hour funding is achievable for strong applications.

Cost: 3/10 - The combination of broker markup, high-risk lender rates, and factor rate products means borrowers at the low end of the credit spectrum face extremely high total costs of capital. The 120%+ APR ceiling is real for weak profiles.

Accessibility: 9/10 - 500 credit minimum with 6-month history is among the most accessible thresholds in the market. This is the only reason to use a marketplace like AFN.

Transparency: 4/10 - Broker incentive structures, factor rate prevalence, and variable lender terms make meaningful comparison difficult without sustained effort from the borrower.

Composite: 6.3 / 10

Reddit reality check

AFN is mentioned less frequently on Reddit than direct lenders, which is itself informative - borrowers who had good experiences tend not to post, while those with rate shock do. The pattern in mentions is consistent: borrowers who used AFN as a last resort after being declined elsewhere are generally satisfied to have received any funding. The complaints focus on receiving MCA offers with factor rates when they expected term loans with APR, and on the follow-up volume from multiple lenders after submitting one application.

Who Advance Funds Network is right for

Good fit: A 5-year-old landscaping company with $130,000 in revenue and a 510 credit score due to a personal bankruptcy two years ago that needs $20,000 for equipment. This borrower has been declined by every direct lender. AFN's network may be the only path to conventional small business funding.

Wrong fit: Any borrower with 600+ credit should approach direct lenders - OnDeck, Fora Financial, SBG Funding - before using a broker. The broker layer adds cost without adding value for borrowers who qualify with direct lenders.

Three things to do before you apply

- Ask AFN explicitly: "Which lenders are in your network, and what is the total cost of capital including any broker fee?" Get the answer in writing.

- Request APR (not factor rate) from every lender offer you receive. If a lender can only quote a factor rate, calculate the implied APR yourself: (factor rate − 1) ÷ loan term in years.

- Apply to at least one direct lender (OnDeck or Fora Financial) in parallel so you have a baseline for comparison.

Read Next

Lender Review

Fora Financial Review: Accessible Capital, at a Price

Independent Fora Financial review - rates, MCA vs. term loan distinction, Reddit sentiment, and who should apply versus look elsewhere.

Lender Review

SBG Funding Review: High Loan Amounts and Multiple Product Options

Independent SBG Funding review - loan amounts up to $5M, qualification requirements, rates, and whether it is a better choice than OnDeck or Fora Financial.

Guide

CDFI Loans Explained: Community Lenders for Businesses Banks Turn Down

CDFI loans fill the gap between bank rejection and business shutdown. Learn what CDFIs are, who qualifies, typical rates, and how to find a CDFI lender in your state.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

See which direct lenders match your credit and revenue profile

Free guide — delivered to your inbox.

Frequently Asked Questions

Answer 10 questions. See which lenders match your profile and what loan types fit.

Check your loan readiness →By FundBizPro Research · Published 2026-05-03 · United States

Written by

FundBizPro Research Team

Backgrounds in commercial banking and SBA lending

The FundBizPro Research Team writes from primary sources - government program documentation, SBA SOP language, lender-published rate sheets, and FDD filings - rather than aggregating other websites. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →