CapFront Review: Lower Rates, Stricter Requirements

TL;DR — Key Facts

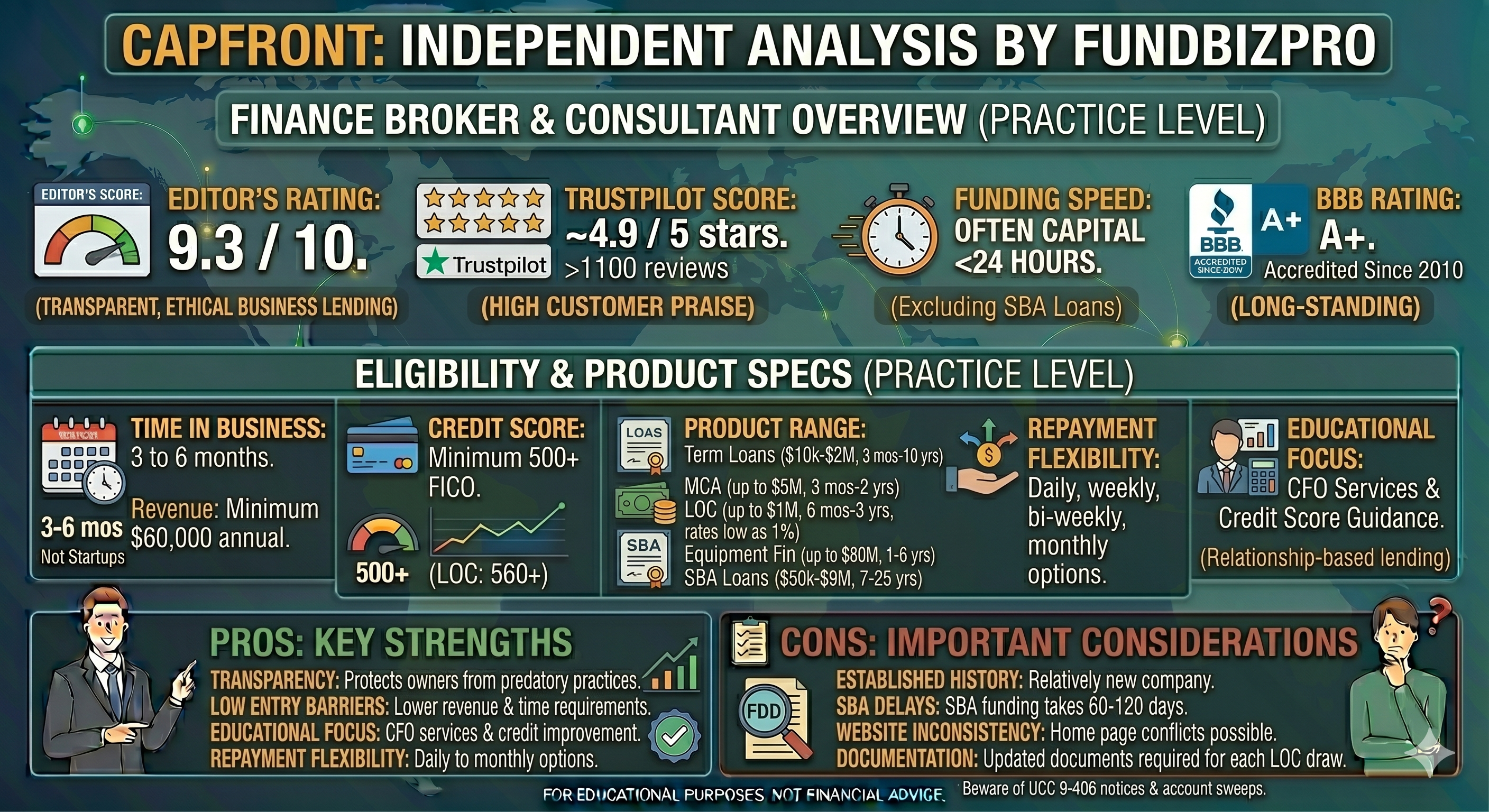

- →CapFront's APR range (12%–65%) is among the most favorable for alternative lenders - lower floor than OnDeck, Fora, or SBG.

- →Minimum requirements: 600 credit score, $180,000 annual revenue, 12 months in business - stricter than most competitors.

- →Loan amounts from $10,000 to $4,000,000; funding in 3 business days.

- →Transparency score of 7/10 - APR is disclosed and terms are clearly documented before signing.

- →Best for established businesses targeting the gap between alternative lenders and SBA approval.

CapFront

United States

Efficiency Score

6.8/10

APR Range

12–65%

Funding

3 days

Min Credit

600+

Verdict

CapFront occupies a distinct position: stricter requirements than most alternative lenders, but meaningfully lower rates as a result. The $180,000 revenue minimum and 600 credit floor will exclude many borrowers who would qualify at OnDeck or Fora. For the businesses that do qualify, CapFront offers one of the better rate environments outside SBA lending - particularly in the 12%–35% APR range that stronger profiles can access.

CapFront at a glance

| Feature | Details |

|---|---|

| Loan amount | $10,000 – $4,000,000 |

| Min credit score | 600 |

| Min annual revenue | $180,000 |

| Min time in business | 12 months |

| APR range | ~12% – 65% |

| Funding speed | 3 business days |

| Origination fee | Yes |

| Prepayment penalty | None |

What the website does not tell you

The $180,000 revenue minimum is the actual barrier. CapFront's stricter revenue requirement ($180K) versus competitors ($100K–$144K) means the lowest-revenue businesses in the alternative lending market won't qualify. The 12-month time-in-business requirement further filters out early-stage operators.

Lower rate floor does not mean everyone gets low rates. The 12% floor is real - but it applies to borrowers with strong credit (680+), multiple years of history, and revenues well above the minimum. A 600 credit score borrower with $185K revenue is likely to receive offers in the 40%–65% range, not 12%.

Equipment financing may have different terms. CapFront advertises equipment financing as a product - which may have different amortization, collateral, and rate structures than working capital loans. If your capital need is equipment-specific, ask for equipment financing terms separately.

FundBizPro Efficiency Score

Speed: 7/10 - 3-business-day funding is competitive but not market-leading. Borrowers who need same-day funding should look at OnDeck.

Cost: 6/10 - The 12%–65% APR range is the most favorable of any alternative lender in this review set. Borrowers who qualify for the lower end of that range are accessing genuinely competitive rates - not just "competitive for alternative lenders."

Accessibility: 7/10 - 600 credit and 12-month minimums are reasonable, but the $180K revenue requirement is the strictest of the lenders reviewed at this credit tier.

Transparency: 7/10 - APR is disclosed upfront, origination fee is disclosed, and terms documentation is clear. One of the higher transparency scores among alternative lenders.

Composite: 6.8 / 10

Reddit reality check

CapFront has limited Reddit discussion compared to OnDeck or Fora Financial - it is less aggressively marketed and serves a narrower (more established) borrower segment. The mentions that exist are generally positive, focusing on lower rates than expected from an alternative lender and professional underwriting. The rare complaint involves the revenue minimum catching borrowers off guard after initial pre-qualification showed promise.

Who CapFront is right for

Good fit: A dental practice with $350,000 in annual revenue, a 650 credit score, and a 3-year operating history that needs $120,000 for equipment upgrades. CapFront's rate environment for this profile (likely 20%–35% APR) is meaningfully better than OnDeck or Fora while still funding in 3 days.

Wrong fit: Startups, businesses under $180K revenue, and borrowers with credit under 600. For these borrowers, Fora Financial (570 minimum) or SBG Funding (550 minimum) are more appropriate. Also wrong for borrowers who can qualify for SBA - the rate differential between 12%–35% alternative and 10%–13.5% SBA is still 5–25 percentage points.

Three things to do before you apply

- Confirm your annual revenue meets the $180K minimum before investing time in the application - this is the most common disqualifier.

- If your credit is 680+ and your revenue is $250K+, also get an SBA pre-qualification: CapFront's lower rate floor is close to SBA rates, but not always better.

- Request the APR in writing before proceeding - CapFront's transparency score is high, but always confirm the specific rate for your profile, not the range.

Read Next

Lender Review

OnDeck Review: Fast Funding with a Real Cost

An independent OnDeck review covering rates (27%–99% APR), qualification requirements, Reddit sentiment, and exactly who should - and should not - use it.

Lender Review

SBG Funding Review: High Loan Amounts and Multiple Product Options

Independent SBG Funding review - loan amounts up to $5M, qualification requirements, rates, and whether it is a better choice than OnDeck or Fora Financial.

Lender Review

Funding Circle Review: The Best Rate Among Alternative Lenders

Independent Funding Circle review - rates (11%–45% APR), strict requirements, US and Canada availability, and who qualifies for the lowest alternative lending rates.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

Check if your business profile qualifies for CapFront's lower rates

Free guide — delivered to your inbox.

Frequently Asked Questions

Answer 10 questions. See which lenders match your profile and what loan types fit.

Check your loan readiness →By FundBizPro Research · Published 2026-05-03 · United States

Written by

FundBizPro Research Team

Backgrounds in commercial banking and SBA lending

The FundBizPro Research Team writes from primary sources - government program documentation, SBA SOP language, lender-published rate sheets, and FDD filings - rather than aggregating other websites. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →