SBA 7(a) Loans for Buying a Business From a Parent

TL;DR — Key Facts

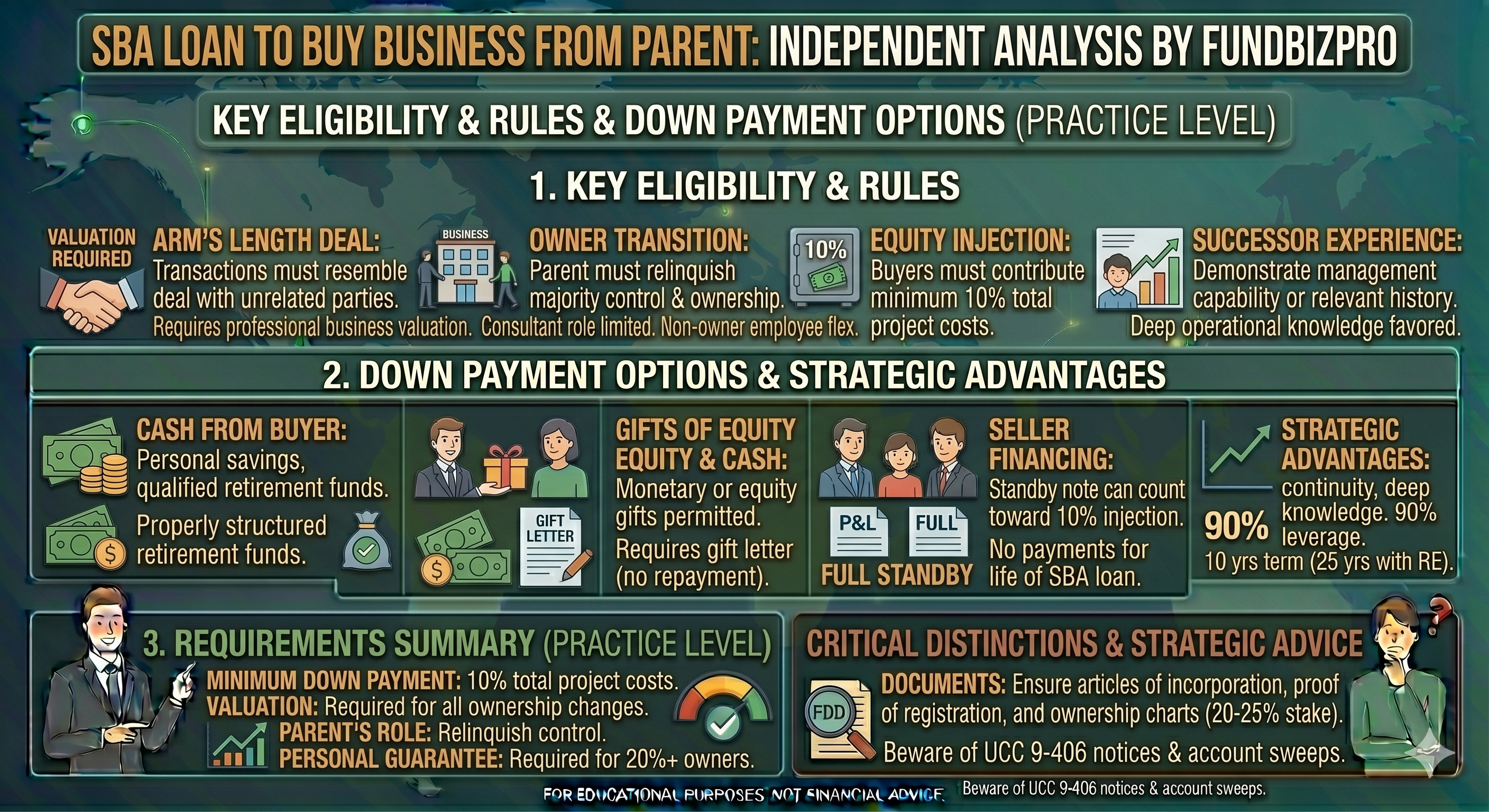

- →SBA 7(a) loans can finance up to 90% of the purchase price in a parent-to-child transfer.

- →The SBA requires fair market value pricing; a discounted family price disqualifies the deal.

- →Minimum equity injection is typically 10%, though lenders often require 20% for family transactions.

- →Seller carry (parent holds a subordinated note) can count toward the equity injection in some structures.

- →Most SBA lenders require 2 years of business tax returns and a third-party business valuation.

Why Intra-Family Transfers Are More Complicated Than They Look

Buying a business from a parent seems straightforward. You know the business, the seller trusts you, and both parties want the deal to work. The complication is the SBA.

The SBA 7(a) program, which finances most small business acquisitions under $5 million, treats family transfers differently than arm's-length sales. The agency's concern is identity-of-interest transactions: deals where the buyer and seller are related enough that the price may not reflect what an independent buyer would actually pay. A purchase price that's artificially low because "it's family" creates a problem: the SBA is guaranteeing a loan secured by collateral that isn't actually worth what the loan says it is.

The practical result: intra-family SBA loans require extra documentation, a qualified third-party business valuation, and a deal structure that passes the arm's-length test. None of this makes the deal impossible. It makes it more paperwork-intensive.

Most SBA-approved lenders handle family transfer deals regularly. The key is starting with a lender experienced in business acquisitions (not a bank that only does real estate) and getting the valuation done before you approach the lender, not after. According to SBA Standard Operating Procedures (SOP 50 10 7.1), lenders must document the arm's-length nature of any acquisition between related parties.

SBA 7(a) Basics for Business Acquisitions

The SBA 7(a) program is the government's primary small business lending vehicle. For acquisition financing, the key parameters are:

| Parameter | Standard 7(a) |

|---|---|

| Maximum loan amount | $5,000,000 |

| SBA guarantee | 85% on loans up to $150K; 75% on loans above $150K |

| Equity injection (buyer) | 10% minimum; lenders often require 15-20% |

| Interest rate (variable) | Prime + 2.75% (loans under $350K); Prime + 2.25% (loans $350K and above) |

| Maximum term (business only) | 10 years |

| Maximum term (with real estate) | 25 years |

| SBA guarantee fee | 0% on loans up to $150K; 0.5-3.5% on larger loans |

*Rates as of early 2026. Verify current Prime rate at federalreserve.gov before modeling any deal.*

For a $1,000,000 business acquisition at Prime + 2.25% (Prime = 7.5%), the fully amortized payment over 10 years is approximately $11,200/month. At a 20% equity injection ($200,000 down), the loan amount is $800,000.

The SBA does not lend directly. It guarantees loans made by approved lenders. Lenders with Preferred Lender Program (PLP) status can approve loans without sending them to the SBA for review, which significantly accelerates closing timelines. For family transfer deals, a PLP lender is worth specifically requesting.

The Arm's-Length Requirement: What It Means in Practice

SBA Standard Operating Procedures (SOP 50 10 7.1) require that acquisitions between related parties, including parent and child, be supported by a third-party business valuation conducted by a qualified appraiser. The valuation must confirm the purchase price is consistent with fair market value.

This creates a specific sequencing requirement for family deals:

1. Get the business valued by a Certified Business Appraiser (CBA) or Certified Valuation Analyst (CVA) before negotiating price 2. Set the purchase price at or near fair market value, not the family discount 3. Present the valuation report to your SBA lender as part of the loan package

If the family wants to offer a below-market price as a gift element, the right structure is usually a split: SBA loan for the fair market value portion, and a gift of equity for the discount. Gifts of equity are not counted as equity injection by most SBA lenders. The overall deal must still pencil at fair market value.

A business appraiser typically charges $3,000-$8,000 depending on business complexity. For businesses with real estate, valuations are higher. This cost is usually financed into the SBA loan as a closing cost. Buyers who skip the appraisal step to save money frequently cause the entire SBA approval to unravel during underwriting.

Seller Carry and Equity Injection Rules

One of the most useful structural tools in a family acquisition is the seller-held note. The parent agrees to receive a portion of the purchase price over time, rather than at closing. This reduces the buyer's cash required at closing and (in some SBA structures) can satisfy part of the equity injection requirement.

The SBA allows seller notes to count toward the equity injection if: - The seller note is fully subordinated to the SBA loan (the SBA lender gets paid first) - The seller note payments are deferred for at least 24 months post-closing - The note does not exceed the equity injection requirement being satisfied

A typical structure for a $1,000,000 family acquisition:

| Component | Amount |

|---|---|

| SBA 7(a) loan | $750,000 |

| Seller-held note (subordinated, 24-month deferral) | $150,000 |

| Buyer cash equity injection | $100,000 |

| Total | $1,000,000 |

In this structure, the buyer injects only $100,000 in cash (10%) and the parent holds a $150,000 note. The SBA lender treats the seller note as acceptable equity because it's subordinated and deferred.

Not all lenders will accept seller notes toward injection. Some require full cash equity from the buyer. Confirm the lender's policy before structuring the deal, not after.

A Representative Parent-to-Child Transfer

A representative transaction from the HVAC services sector illustrates how these pieces fit together.

A buyer in Texas acquired a $750,000 HVAC services business from her father using a Preferred Lender Program SBA 7(a) loan. The business had three years of tax returns showing $280,000 in annual seller's discretionary earnings (SDE). Deal structure: SBA 7(a) loan for $600,000, subordinated seller note for $75,000 (deferred 24 months, at the prevailing AFR), and $75,000 buyer cash injection (10%).

Total monthly debt service after the deferral period: approximately $7,200. Debt service coverage ratio (DSCR): 1.61x, well above the SBA minimum of 1.25x.

The lender required the buyer to have worked in the business for at least 18 months prior to application. The business valuation came in at $755,000. Because the agreed price of $750,000 was within 1% of appraised value, the arm's-length test was easily met. Loan closed in 78 days.

The notable risk: two major commercial accounts represented 38% of the business's revenue. The lender flagged this concentration and required the buyer to document transition plans for those relationships before approval.

What Lenders Look for in Family Transfer Deals

Beyond the standard SBA underwriting criteria (cash flow, credit, collateral), family transfer lenders scrutinize a few additional factors.

Management transition plan. Lenders want to see that the buyer has a credible plan to run the business post-close. If the parent was the sole operator and the child has no documented experience in the business, that's a risk factor. Two to three years of employment in the business before the acquisition significantly improves approval odds.

Business continuity. Key customer relationships, supplier contracts, and employees often attach to the founding owner personally. A lender will want to understand what percentage of revenue is transferable and whether key staff will remain post-sale.

Personal credit. The SBA uses the buyer's personal credit score (typically 650 or higher for approval). Personal financial statements for any individual holding 20% or more ownership are required.

Collateral. SBA lenders must take a first-lien position on all available business assets. For deals with a shortfall in business collateral, lenders may require a lien on personal real estate. This is standard practice for goodwill-heavy businesses, not a warning sign.

A family business attorney is worth the investment in addition to an SBA lender. Family business transfers can have estate planning implications (gift tax, step-up in basis, buy-sell agreement provisions) that go beyond what an SBA loan officer will flag.

For more on choosing between SBA and conventional routes, see SBA 7(a) vs. Conventional Financing for Intra-Family Business Sales.

How We Researched This

This guide references SBA Standard Operating Procedures (SOP 50 10 7.1), which governs identity-of-interest transactions and related-party acquisition requirements. Loan parameter data (rates, terms, guarantee percentages, fees) is sourced from the SBA's official 7(a) program documentation at sba.gov and the Federal Reserve's published Prime rate data. Equity injection guidance follows published SBA SOP requirements and is cross-referenced against published underwriting standards from multiple SBA Preferred Lenders. Appraiser cost estimates reflect published fee ranges from the American Society of Appraisers and the National Association of Certified Valuators and Analysts (NACVA).

*Figures referenced are as of early 2026. Verify current rates and program requirements at sba.gov.*

Read Next

Guide

Seller Financing for Parent-to-Child Business Transfers

How seller financing works in parent-to-child business handoffs: note structures, IRS interest minimums, subordination rules, and why seller carry dominates intra-family deals over bank financing.

Guide

SBA 7(a) vs. Conventional Financing for Family Business Sales

Direct comparison of SBA 7(a) loans vs. conventional bank financing for family business transfers: eligibility, down payment, rates, terms, collateral requirements, and when each structure wins.

Guide

How to Buy a Business: A Step-by-Step Guide for First-Time Buyers

How to buy a business: from sourcing deals to SBA financing and closing. Covers due diligence, franchise resales, location scoring, and key red flags.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

Compare SBA loan structures for your deal size.

Free guide — delivered to your inbox.

Frequently Asked Questions

Before you sign a lease, know what the data says about your address.

Score a franchise location free →By FundBizPro Editorial · Published 2026-05-01 · United States

Written by

FundBizPro Editorial Team

Backgrounds in commercial banking, SBA lending, and franchise industry research

The FundBizPro Editorial Team covers North American franchise costs, FDD analysis, site selection, and acquisition financing. Articles draw on current FDD filings and primary industry sources and are reviewed before publication. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →