SBA 7(a) vs. Conventional Financing for Family Business Sales

TL;DR — Key Facts

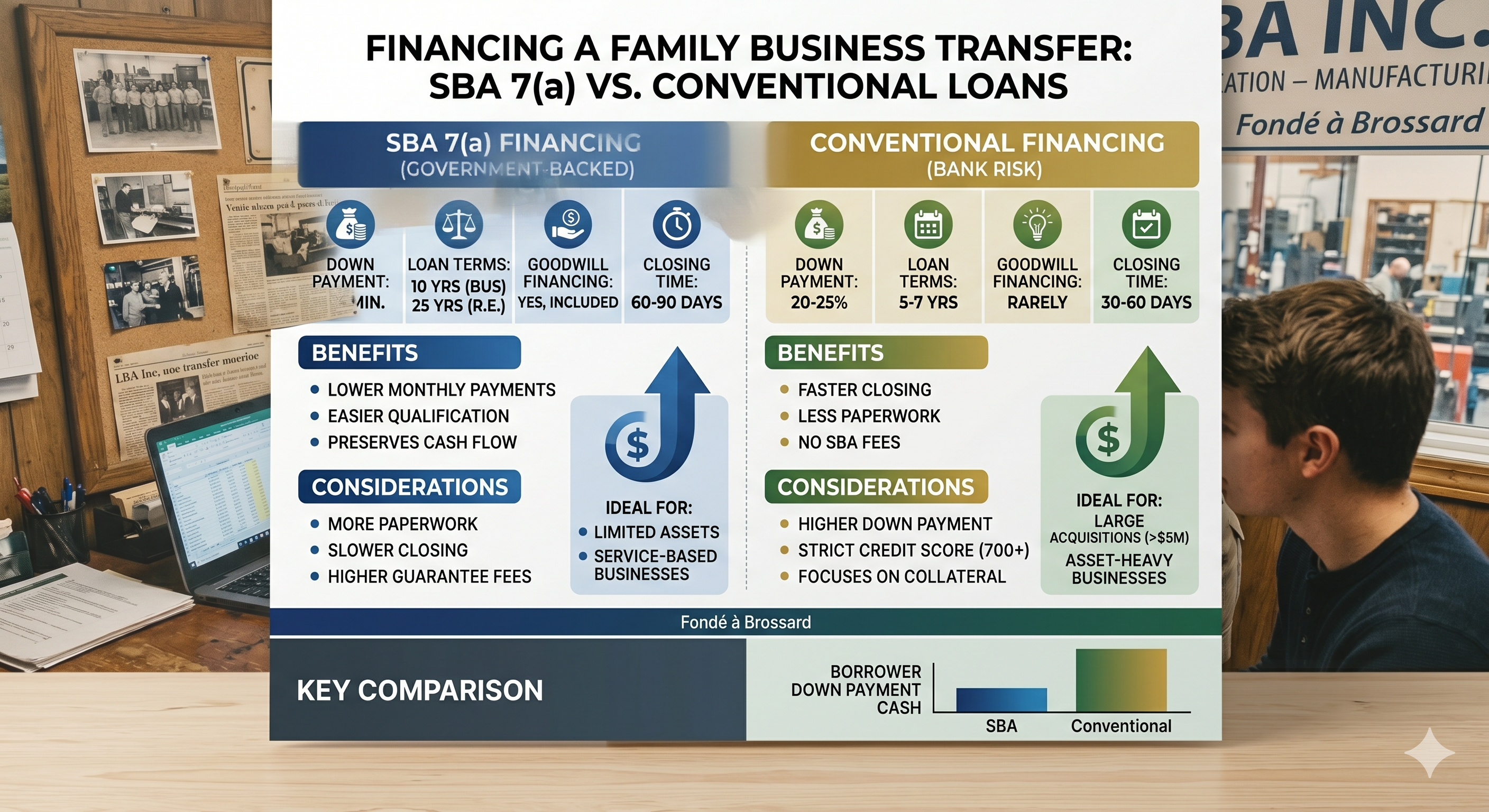

- →SBA 7(a) covers 80-90% of the purchase price; conventional loans typically require 20-30% down.

- →SBA rates (Prime + 2.25-2.75%) are usually lower than conventional business acquisition loans.

- →Conventional loans close faster (30-45 days vs. 60-90 days for SBA).

- →SBA loans carry a guarantee fee of 0.5-3.5% on loans over $150K. Add this to closing cost projections.

- →Goodwill-heavy businesses almost always require SBA financing. Conventional lenders won't finance intangibles.

The Core Difference: What Each Loan Structure Requires

SBA 7(a) loans and conventional business loans both fund small business acquisitions. The difference is who takes the risk when the loan goes bad.

In a conventional loan, the bank underwrites based on the business's collateral and cash flow. If collateral is insufficient, the bank declines. This is the fundamental reason conventional financing is rare in goodwill-heavy business acquisitions: there's not enough physical collateral to back the loan.

In an SBA 7(a) loan, the US Small Business Administration guarantees 75-85% of the loan. The bank's downside is capped. This allows SBA lenders to finance businesses with limited hard collateral, including goodwill, customer relationships, and franchise agreements.

For intra-family business transfers specifically, SBA financing dominates for three reasons: 1. Most small family businesses carry significant goodwill 2. Related-party transactions require additional documentation that SBA lenders are practiced at handling 3. Down payment minimums are lower (10% SBA vs. 20-30% conventional), which matters when the buyer is a child with limited capital

Conventional lenders rarely see family business transfers and often decline them outright rather than navigating the identity-of-interest documentation. That's not a policy judgment against the deal; it's a capacity issue.

Side-by-Side Comparison

| Factor | SBA 7(a) | Conventional Business Loan |

|---|---|---|

| Down payment | 10-20% | 20-30% |

| Maximum loan | $5,000,000 | Varies by lender |

| Interest rate | Prime + 2.25-2.75% (variable) | Prime + 1-4% (variable) or fixed |

| Loan term | 10 years (business only); 25 years (with real estate) | 5-7 years typically |

| Goodwill eligible? | Yes | Rarely |

| Closing timeline | 60-90 days | 30-45 days |

| Guarantee fee | 0-3.5% of guaranteed amount | None |

| Collateral requirement | All business assets + personal lien if gap | Full collateral coverage required |

| Related-party deals | Allowed with valuation | Often declined |

| Seller note toward injection | Yes (if structured correctly) | Usually not accepted |

*Rates as of early 2026. Verify current Prime rate at federalreserve.gov and lender-specific spreads before modeling deal costs.*

When SBA 7(a) Is the Right Choice

SBA 7(a) is almost always the better option for family business transfers when:

The business carries significant goodwill. Service businesses, professional practices, franchise units, and customer-relationship businesses generate most of their value from intangibles that conventional lenders won't finance.

The buyer has limited capital. A 10% equity injection requires half the cash of a 20% down payment on a conventional loan. For a $500,000 acquisition, that's $25,000 vs. $100,000. A meaningful difference for a child taking over a parent's business without a large liquid asset base.

The deal involves a seller-held note. SBA lenders have a defined process for accepting subordinated seller notes toward equity injection. Conventional lenders don't. See Seller Financing for Parent-to-Child Business Transfers for how that structure works.

The business is a franchise. Most SBA-registered franchise brands have pre-approved SBA terms through the Franchise Registry. The SBA loan process for registered franchises is faster and more predictable than for independent businesses.

The seller needs to be bought out at market terms. SBA lenders handle family transfer deals regularly and know the documentation requirements. While closing takes longer than conventional financing, approval rates for qualified applicants are substantially higher.

When Conventional Financing Wins

There are situations where conventional financing is more appropriate than SBA:

The business is collateral-heavy. If the business being transferred has substantial real estate, equipment, or inventory, and that collateral covers the full loan amount, conventional financing avoids the SBA guarantee fee and often closes faster.

The buyer has strong existing banking relationships. A buyer who has banked with a local community bank for 20 years may access conventional business financing with favorable terms that SBA can't match on rate or timeline.

The deal size is under $150,000. For very small family business transfers, the SBA loan process adds documentation burden that may not be worth the benefit. A conventional microloan or CDFI loan may be faster and simpler.

The seller wants a clean break quickly. Conventional loans close in 30-45 days vs. 60-90 days for SBA. If the parent needs to close before a specific estate planning date or year-end, conventional timing may be necessary.

The business is not SBA-eligible. Certain business types are ineligible for SBA financing, including real estate investment companies, financial institutions, and some professional services. Verify eligibility at sba.gov before assuming SBA is an option. This check takes 10 minutes and prevents months of wasted process.

The Guarantee Fee: An Often-Missed SBA Cost

SBA loans carry an upfront guarantee fee that conventional loans don't. This fee is paid to the SBA by the lender and typically passed to the borrower as a closing cost.

| Loan Amount | Guarantee Percentage | Guarantee Fee |

|---|---|---|

| $150,000 or less | 85% guaranteed | 0% |

| $150,001-$700,000 | 75% guaranteed | 3.0% of guaranteed amount |

| $700,001-$1,000,000 | 75% guaranteed | 3.5% of guaranteed amount |

| Above $1,000,000 | 75% guaranteed | 3.5% on first $1M guaranteed; 3.75% above |

For a $500,000 SBA loan (75% guaranteed = $375,000 guaranteed amount), the guarantee fee is 3.0% x $375,000 = $11,250. This is typically financed into the loan, not paid at closing from cash. But it adds to the total loan balance.

Including the guarantee fee in deal modeling is essential. Buyers who compare SBA vs. conventional on rate alone, without including the fee, underestimate the total cost of SBA financing for larger transactions. On a $1,000,000 loan, the guarantee fee can exceed $26,000.

*Guarantee fee amounts are per the SBA's published fee schedule, effective as of early 2026. Verify current fee schedules at sba.gov.*

A Representative Comparison: Same Business, Two Paths

A $900,000 commercial cleaning franchise transfer from mother to son illustrates why most family deals land on SBA.

Business composition: $90,000 in equipment (vacuum systems, vehicles, cleaning equipment), $810,000 in goodwill and customer contracts (92% of total value). The son had managed operations for two years.

Path 1: Conventional bank loan. A regional bank's commercial lending team reviewed the deal and declined. Reason: insufficient collateral. The $90,000 in equipment supported a maximum conventional loan of approximately $63,000 (70% loan-to-value on equipment). The remaining $827,000 needed to close the deal had no acceptable collateral basis for a conventional loan.

Path 2: SBA 7(a) loan. An SBA Preferred Lender approved $720,000 (80%) with a $90,000 cash injection (10%) and a $90,000 subordinated seller note (24-month deferral, 10%). Business DSCR: 1.82x based on three years of tax returns. Guarantee fee: $16,200 (financed into the loan). Closing timeline: 74 days.

The SBA path was the only viable bank financing route for this business. Conventional lenders weren't an option.

How We Researched This

This guide references SBA Standard Operating Procedures (SOP 50 10 7.1) governing 7(a) loan parameters, guarantee percentages, and related-party transaction requirements; published SBA fee schedules (sba.gov/funding-programs/loans/7a-loans); and the Federal Reserve's Prime rate data (federalreserve.gov). Conventional loan comparison data reflects published requirements from community bank and regional bank commercial lending programs. Closing timeline data reflects typical SBA Preferred Lender Program (PLP) processing times as documented by the SBA's Office of Capital Access.

*Figures referenced are as of early 2026. Verify current SBA terms, fees, and eligibility at sba.gov.*

Read Next

Guide

SBA 7(a) Loans for Buying a Business From a Parent

Complete guide to SBA 7(a) financing for intra-family business transfers: eligibility rules, arm's-length requirements, equity injection minimums, and how lenders evaluate parent-to-child deals differently than third-party sales.

Guide

Seller Financing for Parent-to-Child Business Transfers

How seller financing works in parent-to-child business handoffs: note structures, IRS interest minimums, subordination rules, and why seller carry dominates intra-family deals over bank financing.

Guide

Goodwill Financing in Family Business Transfers

How goodwill is valued, financed, and treated in family business acquisitions: SBA rules on intangible collateral, tax allocation elections, and why goodwill creates unique challenges for intra-family deals.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

Compare SBA 7(a) vs. conventional structures for your specific deal size.

Free guide — delivered to your inbox.

Frequently Asked Questions

Before you sign a lease, know what the data says about your address.

Score a franchise location free →By FundBizPro Editorial · Published 2026-05-01 · United States

Written by

FundBizPro Editorial Team

Backgrounds in commercial banking, SBA lending, and franchise industry research

The FundBizPro Editorial Team covers North American franchise costs, FDD analysis, site selection, and acquisition financing. Articles draw on current FDD filings and primary industry sources and are reviewed before publication. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →