Seller Financing for Parent-to-Child Business Transfers

TL;DR — Key Facts

- →Seller financing covers 20-40% of intra-family business deals as the primary or co-primary structure.

- →Seller notes must charge at least the IRS Applicable Federal Rate (AFR) to avoid gift tax treatment.

- →A seller note subordinated to an SBA loan can count toward the buyer's equity injection.

- →Seller notes deferred 24 or more months post-closing are the most SBA-lender-friendly structure.

- →The seller's risk: if the business fails, the note may be uncollectable. Mitigate with collateral and life insurance.

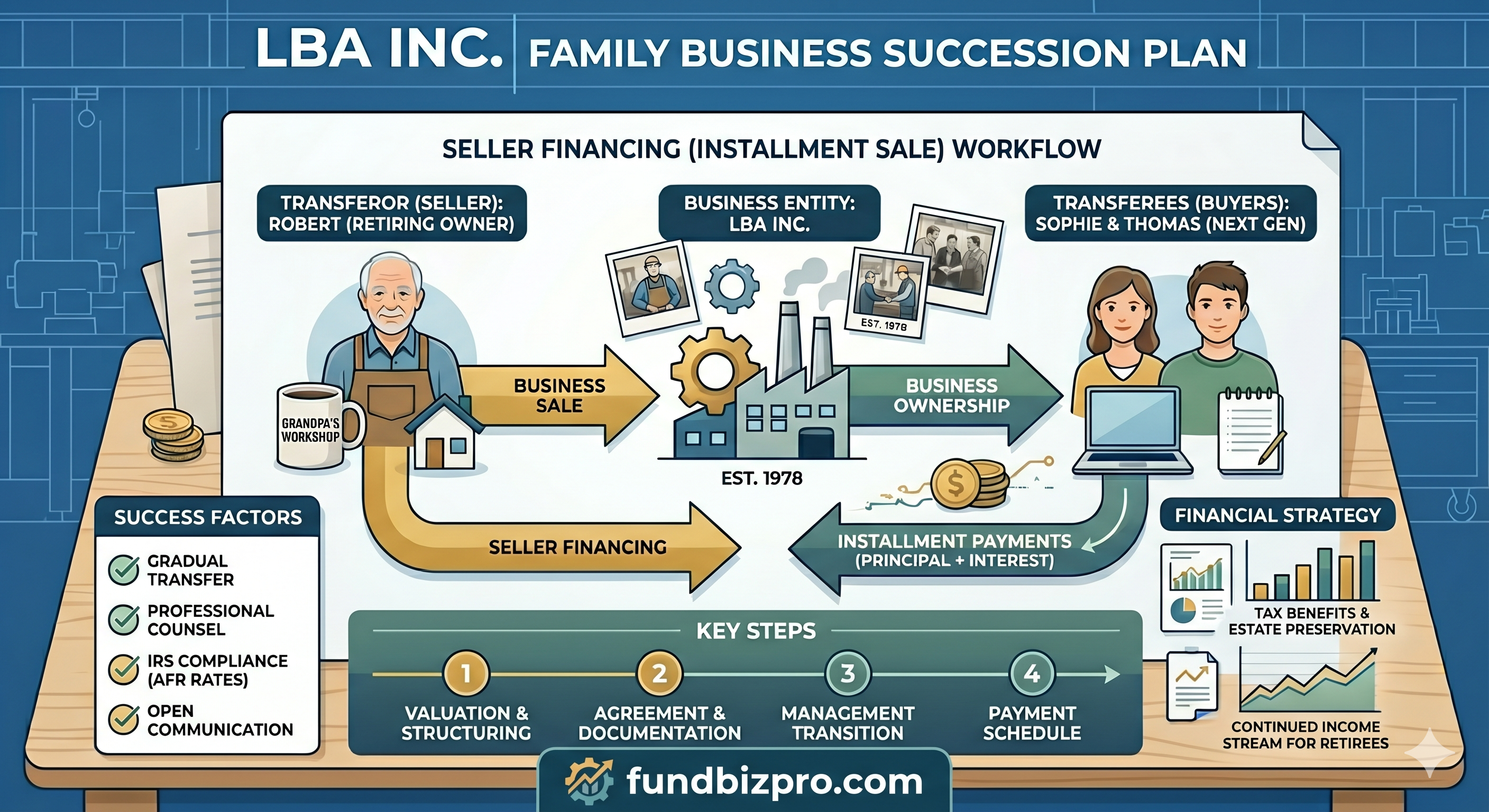

Why Seller Financing Dominates Family Business Transfers

In a third-party business sale, seller financing is a negotiating chip. The seller agrees to carry a note to help the buyer get bank financing approved. In a family transfer, seller financing is often the entire structure.

The reasons are practical. A parent transferring a business to a child usually wants three things: the business to survive the transition without unserviceable bank debt; their child to succeed without a debt load that threatens viability; and a fair price over time, not necessarily a maximum price immediately.

These goals align with seller carry better than with bank financing. A seller-held note gives the parent a stream of income in retirement. It keeps the business debt service manageable for the child. And it avoids the bank qualification hurdles that family deals sometimes struggle with, particularly when the business has modest documentation or the buyer has limited personal financial history.

The tradeoff is risk concentration. The parent's retirement income depends on the business's continued success. If the child runs the business into the ground, the note may be worthless. Proper structuring (collateral, life insurance, and clear default remedies) addresses this risk, but does not eliminate it. Sellers who carry more than they can afford to lose as a worst case are overexposed.

IRS Minimum Interest: The AFR Requirement

Any loan between family members, including a business seller note from parent to child, must charge at least the IRS Applicable Federal Rate (AFR) to avoid imputed income and gift tax complications.

The AFR has three tiers based on loan term:

| Loan Term | AFR Type | Approximate Rate (Early 2026) |

|---|---|---|

| Up to 3 years | Short-term | 4.5-5.0% |

| 3-9 years | Mid-term | 4.3-4.7% |

| Over 9 years | Long-term | 4.5-4.8% |

*Current AFR rates are published monthly at irs.gov/applicable-federal-rates. Verify the current month's rate before closing.*

If the seller note charges below-AFR interest, the IRS treats the below-market interest as a gift from parent to child, which may trigger gift tax reporting. For most family deals, setting the note rate at or slightly above the current AFR eliminates the issue.

The AFR applies to the note rate at origination, not as a floating rate. Most family seller notes use a fixed rate at the prevailing AFR at the time of closing. According to IRS Rev. Proc. 2024-18, short-term and mid-term AFR rates are indexed monthly to Treasury yields.

How Seller Notes Work With SBA Financing

When bank financing is part of the deal, the seller note's subordination structure determines whether the SBA lender will accept it.

A fully subordinated seller note means the seller agrees to receive nothing from their note until the SBA loan is fully repaid. In practice, subordinated notes typically still make regular payments. The subordination clause only triggers if the business defaults or is sold.

SBA lender requirements for seller note acceptance vary but generally follow this framework:

| Requirement | Standard |

|---|---|

| Subordination | Fully subordinated to SBA loan (written standstill agreement) |

| Payment deferral | Payments deferred 24 months post-closing (most lenders) |

| Note term | At least as long as SBA loan term |

| Counts toward equity injection? | Yes, if deferred 24 months and fully subordinated |

A deal structured with a $700,000 SBA loan, a $200,000 subordinated seller note (24-month deferral), and $100,000 buyer cash injection meets the 10% equity injection threshold at most lenders. The seller receives $100,000 at closing (from buyer cash), with the remaining $900,000 paid via SBA loan and seller note over time.

Not every SBA lender will accept seller notes toward equity injection. Some require 100% cash equity from the buyer. Confirming this policy before structuring the deal prevents costly restructuring late in the process.

A Realistic Parent-to-Child Deal Structure

Most parent-to-child business transfers blend seller carry with at least some bank financing. The proportions depend on the business's loan eligibility and the family's financial situation.

A representative structure for a $600,000 business:

| Component | Amount | Terms |

|---|---|---|

| SBA 7(a) loan | $420,000 | 10-year term, Prime + 2.25%, secured by business assets |

| Seller note (subordinated) | $120,000 | 7-year term, AFR rate, 24-month payment deferral |

| Buyer cash injection | $60,000 | 10% equity injection at closing |

Parent receives: - $60,000 at closing - $420,000 from SBA loan proceeds at closing - $120,000 paid over 7 years from business cash flow (deferred 24 months)

Buyer's initial monthly obligation: - SBA loan payment: approximately $4,700/month (months 1-24) - Seller note payment: $0 (deferred)

After the 24-month deferral, the seller note payment (approximately $1,550/month at AFR over the remaining 5 years) is added to the SBA payment. The business needs to service approximately $6,250/month from month 25 onward.

This structure works for a business with $350,000-$400,000 in annual cash flow: manageable debt service plus owner compensation. A business with only $150,000 in annual cash flow would be stressed at these payment levels.

A Representative Transfer: Plumbing Company, Pacific Northwest

A mother transferred a plumbing company to her son in Washington State. Appraised business value: $580,000. The son had worked in the business for four years and held a master plumber license.

Structure: SBA 7(a) loan for $290,000 (50%), subordinated seller note for $232,000 (40%, deferred 24 months at mid-term AFR), and buyer cash injection of $58,000 (10%). The high seller-note proportion reflected the mother's preference to minimize immediate bank debt on the business.

Month 1-24 debt service (SBA only): approximately $3,250/month. From month 25: $3,250 + $2,570 (seller note payment) = $5,820/month total. Business annual SDE: $210,000 ($17,500/month). DSCR from month 25: 3.0x. Well above the SBA's 1.25x minimum.

The deal took 91 days from signed letter of intent to closing. The SBA required a customer concentration analysis because one commercial property management company represented 29% of revenue. The son documented a 5-year contract with that client, which resolved the lender's concern.

Protecting the Seller: Collateral and Default Provisions

The parent holding a seller note is an unsecured or subordinated creditor. If the business struggles, they may wait years to receive payment. Protection measures worth including in the note agreement:

Collateral. A first or second lien on business assets gives the seller recourse. If subordinated to an SBA loan, the seller has second-lien position. Recovery after an SBA lender takes first proceeds is often limited, but it's meaningfully better than no lien at all.

Life insurance. A term life policy on the acquiring child (with the seller named as beneficiary up to the note balance) covers the note if the buyer dies. Annual premium on a 10-year, $200,000 policy for a healthy 40-year-old runs $300-$600/year. A modest cost relative to the risk being covered.

Reporting covenants. Require annual financial statements (tax returns or CPA-reviewed P&Ls) so the seller can monitor business health. Include a provision allowing the seller to accelerate the note if defined financial thresholds aren't met.

Attorney-drafted documentation. A handshake or informal note is not adequate. The note agreement should be drafted by a business attorney and reviewed by both parties independently. For transactions over $200,000, this typically costs $1,500-$3,000.

For more on how seller notes interact with SBA requirements, see SBA 7(a) Loans for Buying a Business From a Parent.

How We Researched This

This guide references IRS guidance on the Applicable Federal Rate (published monthly at irs.gov/applicable-federal-rates per Rev. Proc. 2024-18), SBA Standard Operating Procedures (SOP 50 10 7.1) governing seller note eligibility for equity injection credit, and published SBA 7(a) loan parameters from sba.gov. Deal structure examples reflect documented structures from publicly available SBA lender guidance and NACVA valuation standards. Life insurance premium estimates reflect published actuarial rate ranges for term policies.

*Figures referenced are as of early 2026. Verify current AFR rates at irs.gov and current SBA terms at sba.gov.*

Read Next

Guide

SBA 7(a) Loans for Buying a Business From a Parent

Complete guide to SBA 7(a) financing for intra-family business transfers: eligibility rules, arm's-length requirements, equity injection minimums, and how lenders evaluate parent-to-child deals differently than third-party sales.

Guide

Goodwill Financing in Family Business Transfers

How goodwill is valued, financed, and treated in family business acquisitions: SBA rules on intangible collateral, tax allocation elections, and why goodwill creates unique challenges for intra-family deals.

Guide

SBA 7(a) vs. Conventional Financing for Family Business Sales

Direct comparison of SBA 7(a) loans vs. conventional bank financing for family business transfers: eligibility, down payment, rates, terms, collateral requirements, and when each structure wins.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

Compare SBA 7(a) vs. seller note structures for your deal.

Free guide — delivered to your inbox.

Frequently Asked Questions

Before you sign a lease, know what the data says about your address.

Score a franchise location free →By FundBizPro Editorial · Published 2026-05-01 · United States

Written by

FundBizPro Editorial Team

Backgrounds in commercial banking, SBA lending, and franchise industry research

The FundBizPro Editorial Team covers North American franchise costs, FDD analysis, site selection, and acquisition financing. Articles draw on current FDD filings and primary industry sources and are reviewed before publication. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →