Goodwill Financing in Family Business Transfers

TL;DR — Key Facts

- →Goodwill is typically 40-70% of the purchase price in service businesses with strong customer relationships.

- →Banks won't collateralize goodwill. It requires an SBA loan or seller carry to finance.

- →SBA 7(a) loans can finance goodwill if the business has sufficient cash flow to service the debt.

- →IRS Form 8594 governs how both buyer and seller allocate the purchase price across asset classes at closing.

- →Personal goodwill (attached to the seller individually) may not transfer. Verify before signing.

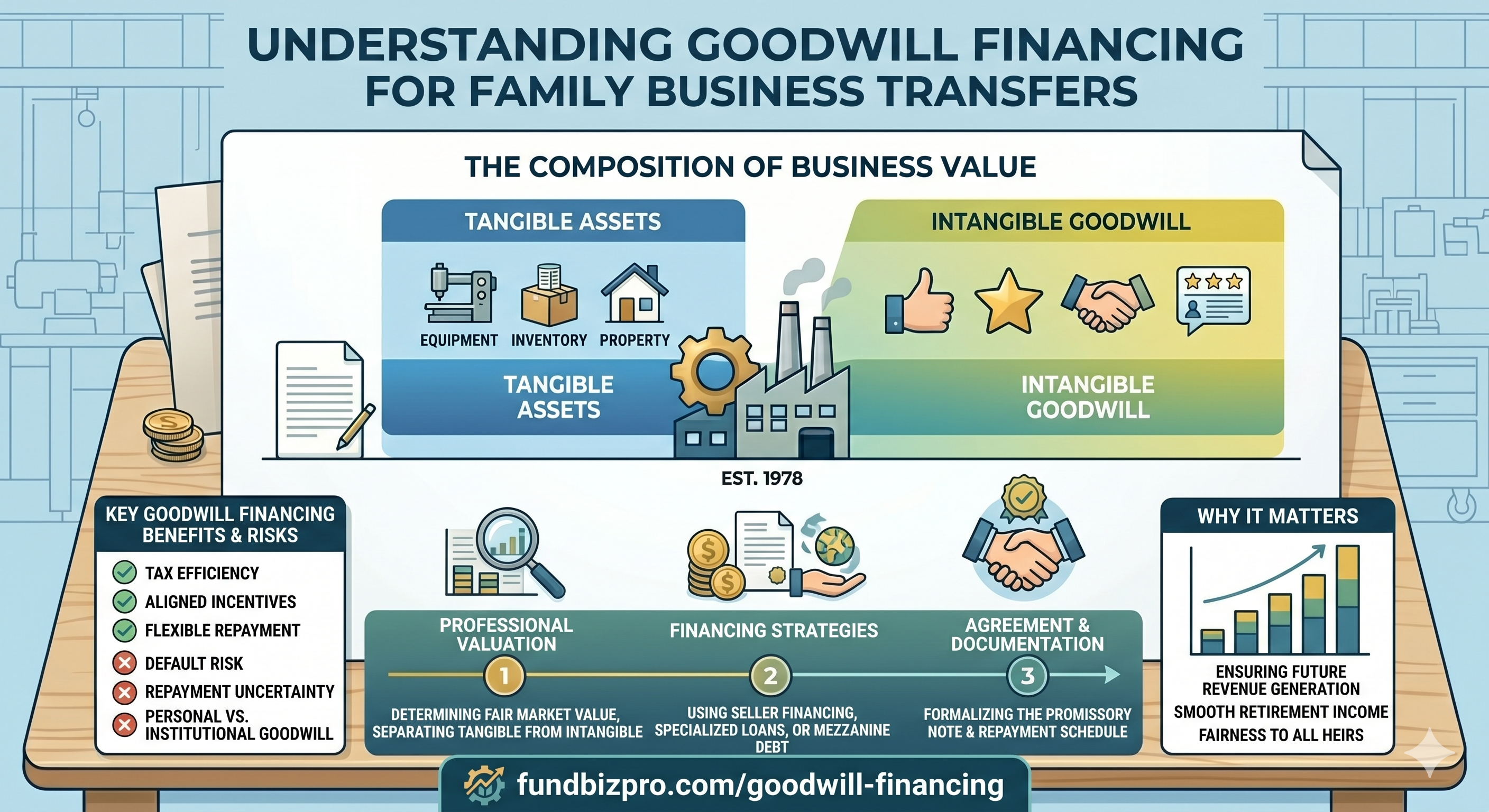

What Goodwill Is and Why It's a Financing Problem

In a business acquisition, goodwill is the amount you pay above the net fair market value of tangible assets. It captures the value of customer relationships, brand reputation, trade secrets, trained workforce, and operating processes: things that generate revenue but can't be touched or seized.

For a service business (accounting practice, dental office, cleaning franchise, consulting firm), goodwill often represents 50-70% of the total purchase price. This creates a specific financing problem: banks won't lend against it.

Conventional bank loans require collateral. Goodwill is not collateral in any meaningful legal sense. If the business fails, a lender who foreclosed on $300,000 of goodwill would find it worthless. There's nothing to sell. This is why goodwill-heavy business acquisitions almost always require either an SBA loan (guaranteed by the government, not secured purely by business collateral) or seller carry.

In a family transfer, where goodwill often represents the bulk of the value a parent spent decades building, this financing structure shapes every aspect of the deal.

How SBA Lenders Handle Goodwill

The SBA 7(a) program explicitly allows goodwill to be financed. The SBA guarantee compensates lenders for the intangible collateral problem. The government backstops the portion the lender can't secure with physical assets.

SBA underwriting of goodwill-heavy deals focuses on cash flow, not collateral. The critical metric is Debt Service Coverage Ratio (DSCR): the business's annual net cash flow divided by total annual debt payments. SBA lenders require a minimum DSCR of 1.25x, per SBA SOP 50 10 7.1.

| Business Net Cash Flow | Annual SBA Loan Payment | DSCR | SBA Eligible? |

|---|---|---|---|

| $120,000 | $80,000 | 1.50x | Yes |

| $100,000 | $80,000 | 1.25x | Borderline |

| $90,000 | $80,000 | 1.13x | No |

For a $600,000 business acquisition financed at 80% SBA ($480,000 loan, 10-year term, Prime + 2.25%), annual debt service runs approximately $67,000. The business needs at minimum $84,000 in annual net cash flow (after owner compensation) to meet the 1.25x DSCR threshold.

When tangible asset collateral falls short (common in goodwill-heavy deals), SBA lenders may require a personal real estate lien from the buyer to partially cover the shortfall. This is standard practice, not a rejection signal.

Personal Goodwill vs. Enterprise Goodwill

One of the most important due diligence questions in any family business transfer is whether the goodwill is personal or enterprise goodwill. Most buyers don't ask this question explicitly, and most sellers have no incentive to raise it.

Enterprise goodwill attaches to the business itself: its brand, systems, customer contracts, and location. It transfers with the business when the owner changes. A well-documented franchise unit with trained staff and a signed lease carries enterprise goodwill.

Personal goodwill attaches to the specific individual running the business. A dental practice where patients come specifically because they trust the founding dentist, a law firm where clients follow the lead partner, or a family restaurant where regulars come for the founder's cooking: these have significant personal goodwill. When the founder leaves, a portion of that goodwill may leave with them.

For family transfers, the test is practical: will customers stay when the child takes over? If the parent had a 30-year relationship with every major client, and those clients have never met the child, personal goodwill risk is high.

Buyers should request customer concentration data: what percentage of revenue comes from the top 5, top 10 clients? Are clients on transferable agreements or on a handshake? Lenders ask these same questions when underwriting goodwill-heavy deals. Answers that aren't in writing don't count.

Tax Allocation: IRS Form 8594

When a business is sold in an asset purchase (the most common structure for small business acquisitions), both buyer and seller must file IRS Form 8594, which allocates the purchase price across seven asset classes. The allocation determines each party's tax outcome.

| Asset Class | Buyer Benefit | Seller Preference |

|---|---|---|

| Class I: Cash and cash equivalents | Neutral | Neutral |

| Class II: Securities | Ordinary income to seller | Neutral |

| Class III: Accounts receivable | Ordinary income to seller | Neutral |

| Class IV: Inventory | Ordinary income to seller | Neutral |

| Class V: Equipment and furniture | Depreciable, 5-7 year | Capital gains |

| Class VI: Intangibles (non-compete, customer lists) | Amortizable, 15 years | Ordinary income |

| Class VII: Goodwill | Amortizable, 15 years | Capital gains |

Goodwill (Class VII) is the most favorable asset class for sellers: it generates long-term capital gains. For buyers, goodwill is amortizable over 15 years under IRC Section 197, generating a tax deduction that partially offsets the purchase cost.

Buyers prefer allocations weighted toward Class V (equipment, faster depreciation) and away from goodwill (15-year amortization is slow). Sellers prefer goodwill for capital gains treatment. In a family transfer, this allocation negotiation still matters, especially when there's a tax advisor for each party. Both parties must file consistent allocations. Inconsistent Form 8594 filings between buyer and seller trigger IRS scrutiny.

Structuring the Deal When Most of the Value Is Goodwill

A service business worth $800,000 might have only $50,000 in equipment and $10,000 in receivables. The remaining $740,000 is goodwill: intangible value with no collateral. How do you finance that?

Structure 1: SBA-led SBA 7(a) for $640,000 (80%), seller note (subordinated, 24-month deferral) for $80,000, buyer cash injection $80,000 (10%). Works if business DSCR is 1.25x or higher on the full debt load. Buyer needs strong personal credit and personal real estate for collateral shortfall.

Structure 2: Seller-carry primary Parent carries $600,000 as a seller note at AFR; buyer injects $200,000 cash. No bank involved. Monthly payments lower, but parent holds the risk. Appropriate when parent doesn't need immediate liquidity and wants to support a smooth transition.

Structure 3: Partial SBA + earn-out SBA for $400,000 on tangible assets plus working capital; earn-out for $400,000 of goodwill value (paid at 15% of annual revenue for 10 years, capped at $400,000). Aligns goodwill payment with actual performance. If the goodwill doesn't transfer to the child, the payout is reduced accordingly.

Structure 3 is underused and well-suited to situations where personal goodwill risk is high. The earn-out structure makes the seller's payout contingent on their reputation actually surviving the transition.

For more detail on how seller notes interact with SBA structure, see Seller Financing for Parent-to-Child Business Transfers.

A Representative Goodwill-Heavy Acquisition

A certified public accounting practice in Colorado sold from father to daughter for $820,000. Tangible assets: $45,000 in office equipment and furniture. The remaining $775,000 was goodwill (94.5% of total value).

Financing: SBA 7(a) loan for $656,000 (80%), buyer cash injection $82,000 (10%), subordinated seller note $82,000 (24-month deferral, mid-term AFR). The lender required a personal real estate lien to bridge the collateral gap between the $45,000 in tangible assets and the $492,000 SBA collateral requirement on a 75%-guaranteed $656,000 loan.

Key underwriting issue: 7 long-term clients represented 61% of revenue. The daughter had worked at the practice for 3 years and had existing relationships with all 7. The lender required signed letters of intent to continue from 5 of the 7 clients before issuing conditional approval.

Time from letter of intent to closing: 103 days, extended by the client letter process. The deal closed. Within 18 months, the daughter had retained all 7 clients and added 4 new ones through referrals.

How We Researched This

This guide references IRC Section 197 (intangible amortization, 15-year schedule for goodwill), IRS Form 8594 instructions (Asset Acquisition Statement, asset class definitions), SBA Standard Operating Procedures (SOP 50 10 7.1) governing DSCR requirements and collateral shortfall handling, and standard business valuation methodology from the American Society of Appraisers. The DSCR table reflects published SBA underwriting minimums. Tax class allocation guidance is sourced from IRS Form 8594 instructions, publicly available at irs.gov.

*Figures referenced are as of early 2026. Consult a CPA for current IRS rates and amortization rules. Verify SBA DSCR requirements at sba.gov.*

Read Next

Guide

SBA 7(a) Loans for Buying a Business From a Parent

Complete guide to SBA 7(a) financing for intra-family business transfers: eligibility rules, arm's-length requirements, equity injection minimums, and how lenders evaluate parent-to-child deals differently than third-party sales.

Guide

Seller Financing for Parent-to-Child Business Transfers

How seller financing works in parent-to-child business handoffs: note structures, IRS interest minimums, subordination rules, and why seller carry dominates intra-family deals over bank financing.

Guide

SBA 7(a) vs. Conventional Financing for Family Business Sales

Direct comparison of SBA 7(a) loans vs. conventional bank financing for family business transfers: eligibility, down payment, rates, terms, collateral requirements, and when each structure wins.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

Understand SBA 7(a) financing options for your acquisition.

Free guide — delivered to your inbox.

Frequently Asked Questions

Before you sign a lease, know what the data says about your address.

Score a franchise location free →By FundBizPro Editorial · Published 2026-05-01 · United States

Written by

FundBizPro Editorial Team

Backgrounds in commercial banking, SBA lending, and franchise industry research

The FundBizPro Editorial Team covers North American franchise costs, FDD analysis, site selection, and acquisition financing. Articles draw on current FDD filings and primary industry sources and are reviewed before publication. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →