Funding Circle Review: The Best Rate Among Alternative Lenders

TL;DR — Key Facts

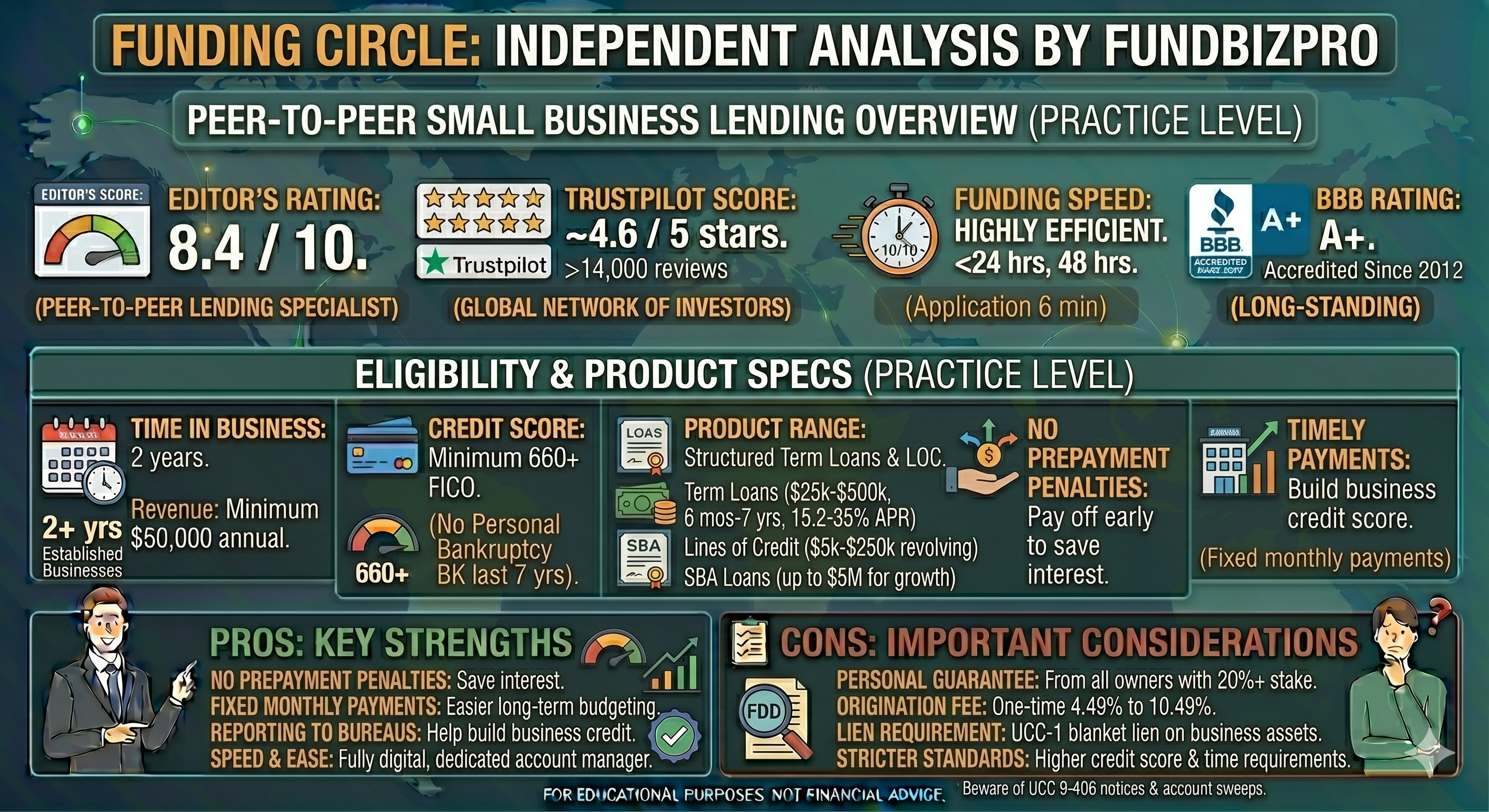

- →Funding Circle's APR range (11%–45%) is the lowest of any alternative lender reviewed - competitive with SBA 7(a) at the low end.

- →Minimum requirements: 660 credit score, $150,000 annual revenue, 24 months in business - the strictest of all lenders reviewed.

- →Available in both the US and Canada (as separate programs).

- →Loan amounts from $25,000 to $500,000; funding in 5 business days.

- →Origination fee applies; no prepayment penalty.

Funding Circle

US & Canada

Efficiency Score

6.8/10

APR Range

11–45%

Funding

5 days

Min Credit

660+

Verdict

Funding Circle is the best-priced alternative lender in this review set - 11%–45% APR puts its low end in the same range as SBA preferred lenders, with approval in 5 days rather than 45. The trade-off is the strictest minimum requirements: 660 credit, 24 months in business, and $150,000 in revenue. For the businesses that qualify, Funding Circle represents a genuine alternative to SBA lending when speed matters. For everyone else, it is simply out of reach.

Funding Circle at a glance

| Feature | Details |

|---|---|

| Loan amount | $25,000 – $500,000 |

| Min credit score | 660 |

| Min annual revenue | $150,000 |

| Min time in business | 24 months |

| APR range | ~11% – 45% |

| Funding speed | 5 business days |

| Origination fee | Yes |

| Prepayment penalty | None |

What the website does not tell you

The 24-month requirement is a hard wall. Unlike some lenders who show 24 months as a preference, Funding Circle enforces it as a minimum. Businesses under 2 years old will not be approved regardless of revenue or credit.

US and Canadian operations are separate programs. Funding Circle operates distinct programs in the US and Canada. The rates, amounts, and requirements differ between the two markets. Borrowers in Canada should verify Canadian-specific requirements rather than applying based on US program details.

The origination fee matters at this rate level. At 11%–15% APR, even a 2.5%–4% origination fee represents a meaningful addition to the total cost. On a $200,000 loan, a 3% origination fee adds $6,000 to the cost of borrowing - which at 11% APR represents roughly half a year of interest. Factor this into the comparison with SBA lenders, which also charge origination but at different rate levels.

FundBizPro Efficiency Score

Speed: 6/10 - 5-business-day funding is slower than most alternative lenders. Not SBA-slow (45–90 days), but not same-day either. If you need capital in 48 hours, OnDeck is the right choice.

Cost: 7/10 - 11%–45% APR is exceptional for a non-bank lender. The lower end of this range is genuinely competitive with SBA preferred lenders. Even at 30%–40%, this is 20–60 percentage points below OnDeck or Fora Financial for comparable loan amounts.

Accessibility: 6/10 - 660 credit, 24 months, $150K revenue. The strictest requirements of any alternative lender reviewed. This lender serves established, creditworthy businesses only.

Transparency: 8/10 - Funding Circle consistently scores high on transparency across third-party assessments. APR is disclosed clearly, terms are documented, and the underwriting process is communicated to borrowers.

Composite: 6.8 / 10

Reddit reality check

Funding Circle is frequently mentioned in r/smallbusiness threads comparing online lenders for established businesses. The consistent praise: competitive rates and professional underwriting that feels more like a bank than an alternative lender. The consistent complaint: the 24-month minimum is surprising to borrowers who expected to qualify based on revenue and credit alone. No significant fraud reports or systemic service failures appear in community discussions.

Who Funding Circle is right for

Good fit: A B2B services company with 3 years of operating history, $280,000 in annual revenue, and a 690 credit score that needs $150,000 for expansion. This borrower qualifies for Funding Circle's lower rate range and will pay substantially less than with OnDeck or SBG Funding - while still receiving capital in a week rather than two months.

Wrong fit: Any business under 24 months old, any borrower with credit below 660, or any business with revenue under $150K. These borrowers will be declined. Also worth noting: if you have 680+ credit and can wait 6 weeks, SBA preferred lenders will match or beat Funding Circle's rates with government-backed terms.

Three things to do before you apply

- Confirm you have at least 24 calendar months of verifiable operating history - this is the most common disqualifier and Funding Circle enforces it strictly.

- Compare your Funding Circle offer against an SBA pre-qualification: if you qualify for both, the SBA rate may be slightly better and the term longer.

- For Canadian borrowers: verify Funding Circle's current availability in your province, as program availability varies.

Read Next

Lender Review

CapFront Review: Lower Rates, Stricter Requirements

Independent CapFront review - rates (12%–65% APR), qualification requirements, efficiency score, and how it compares to OnDeck and SBG Funding.

Lender Review

SBG Funding Review: High Loan Amounts and Multiple Product Options

Independent SBG Funding review - loan amounts up to $5M, qualification requirements, rates, and whether it is a better choice than OnDeck or Fora Financial.

Financing

SBA 7(a) Loan Explained: Requirements, Rates, and the Real Timeline

The small business administration 7(a) loan goes up to $5 million. Here's what rates look like, who qualifies, and how to cut the 60–90 day timeline.

This article is for informational purposes only and does not constitute financial, legal, or investment advice - consult a licensed professional before making acquisition or financing decisions.

Check if your business qualifies for Funding Circle's lower rates

Free guide — delivered to your inbox.

Frequently Asked Questions

Answer 10 questions. See which lenders match your profile and what loan types fit.

Check your loan readiness →By FundBizPro Research · Published 2026-05-03 · US & Canada

Written by

FundBizPro Research Team

Backgrounds in commercial banking and SBA lending

The FundBizPro Research Team writes from primary sources - government program documentation, SBA SOP language, lender-published rate sheets, and FDD filings - rather than aggregating other websites. Content is educational only and is not a substitute for advice from a licensed professional.

About our editorial standards →